Cite report

IEA (2020), Coal 2020, IEA, Paris https://www.iea.org/reports/coal-2020, Licence: CC BY 4.0

Report options

Trade

Introduction

International coal trade is hit by the pandemic and trade patterns continue to shift to Asia

Global coal trade reached its highest volume ever in 2019 at 1 445 Mt, a 0.8% increase from the previous year1. Trade accounted for 19% of global coal consumption in 2019. Trade in thermal coal (which includes lignite and some anthracite in this section) increased 1.1% while metallurgical (met) coal trade volumes were stable. Thermal coal accounted for 76% of global coal trade and met coal for the rest. The vast majority of coal traded in 2019, 92% (1 331 Mt), was seaborne trade.

Patterns of international (thermal) coal trade are shifting. Traditionally trade could be characterised by two geographic basins: the Pacific Basin, where Japan and Korea were the top importers; and the Atlantic Basin, where the European countries imported most of the traded coal. South Africa, and to a much lesser extent Russia, linked the two basins in coal trade. This no longer portrays international coal trade patterns, as the Atlantic market has separated from Asian market. For instance, in 2019, the volume of coal imports in India were almost double EU import quantities, a clear indicator of a shift to Asia and the waning of Europe in international coal markets.

Indonesia remained the world’s largest exporter of coal (by weight) with total exports of 455 Mt in 2019. Australia ranked second, at 395 Mt, although it remains at the top of the league table ranked by energy and economic values. China was the largest importer of coal in 2019 at 308 Mt, followed by India at 249 Mt.

It is estimated that for 2020 trade volumes will recede around 10%, or around 150 Mt, the largest drop ever, most of which are seaborne coal trade. Trade volumes of thermal coal are expected to decline by 10% and those for met coal by 12%. The largest exporters bear the brunt of the largest absolute decline in exported volumes: Indonesian exports are expected to drop by 51 Mt (-11%) and those from Australia by 30 Mt (-8%). The biggest absolute decrease in imports is in India (-41 Mt). Among significant importers only Viet Nam (+18%, +8 Mt) and maybe Turkey will increase their coal imports.

In 2021, as coal demand recovers, traded volumes will rebound as well. Compared to 2020, exports are expected to increase by 31 Mt (2.4%) to 1 323 Mt in 2021, an increase in seaborne coal trade accounting for 26 Mt. This means that export volumes will remain well below the pre-Covid volumes. The recovery is supported by more imports in India (+12 Mt) and Southeast Asia (+10 Mt). It is expected that Australia and Indonesia in particular will benefit from this recovery in import demand. Australian coal exports are expected to increase by 20 Mt and Indonesian exports by 6 Mt.

Covid-19’s strong impact on coal trade

Thermal coal

Thermal coal trade breaks the record in 2019…

In 2019, 1 093 Mt of thermal coal were traded internationally setting a new volume record. This was up 12 Mt from 2018 though is a much slower growth rate than the previous two years. Approximately 1 021 Mt (94%) of this trade was seaborne. Internationally traded thermal coal as a share of global consumption was stable at 17%.

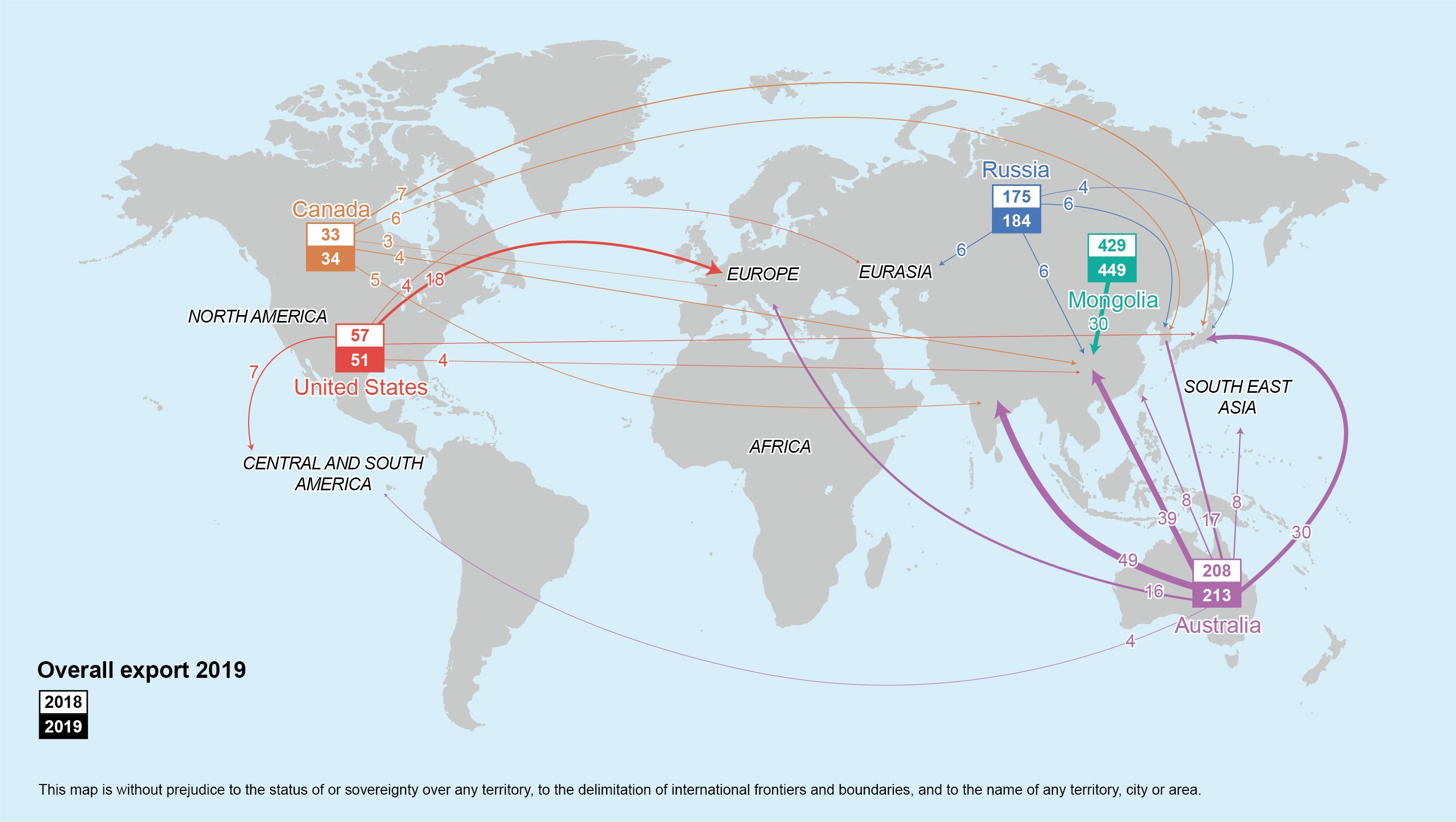

The majority of seaborne thermal coal trade occurs in the Asia Pacific region, where both the largest importers and exporters are concentrated. Indonesia provided 41% of globally traded thermal coal in 2019, and has potential to increase its market share. Australia ranked second with 19%. Other important market participants include Russia (17%), South Africa (7%), Colombia (6%) and the United States (3.1%).

China was the largest importer of thermal coal in 2019 accounting for 21%, followed by India (17%) and Japan (13%). Southeast Asia and Europe each accounted for around 11% of thermal coal imports. Southeast Asia expanded imports by 19% in 2019, as demand from coal-fired electricity generation increased, especially in Viet Nam. Imports to India increased by 12%, despite a decline in overall coal demand. Imports in Japan were slightly lower (-1.6%), sustained by the slow restart of its nuclear power generation capacity. Coal imports to the European Union fell dramatically by 30 Mt (-21%).

Indonesia, Australia and Russia significantly increased their coal exports in 2019. Indonesia and Russia continued to build on their export growth of the previous two years. Indonesia’s coal exports increased by 20 Mt (+4.7%) as production capacity has significantly expanded. Russia increased exports by 9 Mt (+5.0%), though its exports to the European Union decreased by 3 Mt. However, measured against the slump in EU demand, Russia, as a low cost supplier, was able to increase its market share in Europe from around 53% to 65%. In addition, exports to China, India and Southeast Asia expanded. Australian exports increased by 5 Mt (+2.5%), being the main beneficiary of increased imports in Viet Nam. Coal exports through the port of Newcastle, in South Wales (the world’s largest coal exporting port outside China) reached a record of 165 Mt in 2019, around 87% of which was thermal coal.

In relation to the drop in coal imports in the European Union in 2019, exports from Colombia declined by 12 Mt (-15%) and from the United States by 15 Mt (-31%). For the United States, coal exports to India and Korea also fell.

South African exports were relatively stable (-1.8%). As imports declined in Europe and other African countries, South African exports continued to shift to India, Pakistan and Southeast Asia.

… and remains concentrated in the Asia Pacific Basin

Main trade flows in the thermal coal market, 2019 (Mt)

Open

{kind=link}

Thermal coal trade was rattled by the pandemic

Thermal coal import volumes of 987 Mt estimated for 2020 will be about 9% (103 Mt) lower than the previous year. Forecast for 2021 anticipates a recovery of about 4 Mt.

It was expected that the implementation of the IMO-2020 to limit sulphur in shipping fuel in January 2020 would affect international trade2. What was not expected are the consequences of the Covid-19 crisis and how they impact international coal trade.

Imports of thermal coal to Japan, Korea and Chinese Taipei will decline in 2020. In each country, import volumes are driven primarily by demand for thermal coal to generate electricity. With lower electricity demand in 2020, Japan’s thermal coal imports look to decline by 8 Mt, Korea’s by 10 Mt and Chinese Taipei’s by 6 Mt. Although a partial recovery in electricity demand is expected in 2021, the underlying decline in coal-fired power generation in favour of renewable generation persists and gas competition remains as a threat for coal. Japan’s thermal coal imports in 2021 are expected to remain at 2020 levels while Korea’s and Chinese Taipei’s imports are expected to decrease further.

Imports of thermal coal to Viet Nam are expected to increase by 8 Mt (+21%) in 2020 to serve rising demand in the power sector as well as for industrial production. For 2021, a further increase of coal imports of 5 Mt (+11%) is expected as domestic production cannot satisfy increasing demand.

The European Union is playing a significant role in reshaping coal trade patterns. A strong decrease in imports by 24 Mt (-31%) is expected for 2020, a continuation of the trend from the previous year. Imports of thermal coal are expected to decrease in Germany (-7 Mt), Italy (-2 Mt) and Spain (-4 Mt). Since a recovery in coal demand in the European Union is not expected for 2021, import volumes are likely to be unchanged.

Turkey, where imports in 2020 might increase compared with 2019, consolidates its position as the largest thermal coal importer outside the Asia Pacific region, which it assumed after having surpassed Germany in 2018.

Policies to protect domestic coal production rein in imports

Annual coal import quotas have been enforced in recent years in China. Correspondingly, China’s import volatility has jumped. In December 2019, for example, Chinese thermal imports were 1 Mt, plummeting from 14.6 Mt in November 2019 before jumping up again to 26.5 Mt in January 2020. Imports remained high in the first-quarter of 2020 as production in China was disrupted and global coal prices dropped. Towards the middle of 2020 the national government tightened import restrictions to shore up domestic coal producers. In addition, delays in the ports became frequent. As a result, a decrease in thermal coal imports of 19 Mt (-8%) in China is expected for the full year, although the fourth-quarter, and in particular December, is quite uncertain as the import quotas are not known. For 2021, it is expected that China’s thermal coal imports will be similar to 2020 levels, as policies to curtail imports continue.

In response to the domestic decline in demand and rising stockpiles in 2020, India's state-owned coal producer, CIL, is pursuing the goal of replacing thermal coal imports with domestic production. The government mandated the company to replace at least 100 Mt of imports with domestically produced coal in fiscal year 2020-21. In September 2020, CIL announced the Special Spot e-Auction for importer substitution, which aims to replace 150 Mt of coal imports with domestic supply. The CIL sale efforts focus on Indian utilities as well as companies in the cement, sponge iron and fertiliser industries. Any company or trader that imported coal in the current or last two fiscal years is eligible to participate in the auctions.

As a result of the decline in demand and the efforts to replace imports, thermal coal imports to India are expected to decline by 31 Mt for 2020, the largest drop among thermal coal importers. In September 2020 the India’s coal and trade ministers discussed the idea of setting up a coal import monitoring system. This step is in line with government policies to discourage coal imports as a way to support domestic coal sales and reduce the import bill.

India's thermal coal imports are expected to recover only by 5 Mt in 2021 owing to stockpiles built up in 2020, in combination with a potential increase in production and the continuation of policies to discourage imports.

Thermal coal exporters in 2020: A battle about location, quality and costs… and China

Driven by weaker demand and lower prices in 2020, thermal coal exports are expected to fall by 110 Mt (-10%). In 2021 a recovery in exports of 8 Mt is projected. The share of seaborne traded thermal coal remains constant at around 94%.

In absolute numbers, Indonesia is the hardest hit with exports of thermal coal in 2020 decreasing by around 51 Mt (-11%). Indonesian producers in particular are affected by shrinking import demand in Asia, since many mines are high cost producers of low quality coal. Furthermore the country is highly exposed to the Indian market, which is shrinking dramatically in 2020. In 2021 a recovery in exports of 6 Mt is estimated, but it depends on China and India, which accounted for 33% and 27% of Indonesian exports in 2019.

Australian exports of thermal coal are less affected by decreased import demand than Indonesia. Low coal prices in mid-2020 combined with recovering fuel prices and high labour costs mean that many thermal coal mines in Australia have been operating at a loss. High fixed costs of mine operation and take-or-pay contracts for the use of rail and port infrastructure cause most producers to continue operations, as long as the value of take-or-pay costs are higher than losses in production. In addition, term contracts, especially with Japanese utility buyers, support the production of Australian coal when spot prices go below contracted prices. Japan’s fiscal year 2020-21 contract price for high calorific thermal coal settled at USD 68.75/t, significantly higher than mid-year spot prices. Australia was the only major exporting country to increase supply in the first-quarter 2020, driven by strong demand in China at that time. A decline of around 14 Mt (-7%) is expected for 2020 overall with a recovery of 6 Mt in 2021.

Even Russian exports of thermal coal – the growth story of recent years – are expected to fall by about 7 Mt (-3.9%) in 2020, as import demand shrinks in its most important export markets, Europe and Korea. The other two main exporters of thermal coal to Europe are also severely hit by the decline in demand. Exports of the relatively high cost producers of the United States are expected to decline by 12 Mt (-37%), while Colombia’s exports are projected to decline by 13 Mt (-19%). Recovery of previous coal export volumes in 2021 is not expected for these three countries as demand in the Atlantic Basin will remain subdued and a shift of exports to the Asia Pacific region could prove difficult due to the relatively high costs of production and transport. However, if difficulties of Australian coal exports to gain access to Chinese markets persist, unusual coal flows could become the new normal in 2021.

South Africa’s exports are expected to decrease by 5 Mt in 2020. Its exports are generally competitive and well diversified. A combination of quality and price suits sponge iron producers in India, its largest market. In 2021 exports are expected to recover only slightly.

Will 2019 be the peak of thermal coal trade?

Metallurgical coal

Metallurgical coal trade is more concentrated than thermal coal, with Australia leading exports

Although the metallurgical (met) coal market has only one-third the volume of the thermal coal market, international trade plays a more important role for met coal. In 2019, about 352 Mt or 32% of total met coal consumption was met by imports, of which 310 Mt (88%) was seaborne. The market for met coal is highly concentrated on the export side, with Australia (52% share in 2019, 59% if only seaborne is considered) as the dominant global supplier. Other countries with a significant market share include the United States (14%), Canada (10%), Russia (9%) and Mongolia (9%).

Asia Pacific countries accounted for 73% of all met coal imports in 2019, with China leading the way at 24%. China increased imports in comparison to 2018 by 11 Mt (+16%). Imports also increased to India (+2.4%) and Southeast Asia (+31%). China’s import demand was fuelled by relatively low seaborne prices for met coal compared with Chinese domestic prices and increased steel output. Europe as a whole remained one of the largest importers because of its large iron and steel production capacities and shortage of domestic met coal supply, accounting for 18% of all imports. Yet, imports to Europe decreased by 3 Mt (-5%) in 2019, as reduced steel capacity cut demand.

A quarter of Australian met coal exports in 2019 were destined for India. Other major markets for Australian met coal include China with a share of 21% and Japan (17%). Australian exporters benefited from the increase in import demand in China, India and Southeast Asia in 2019. Australian exports increased by 3 Mt (+1.9%).

Mongolian coal producers are limited in their ability to export due to the country's geographical location. Coking coal exports are transported to China via truck. Mongolian exports are particularly price-sensitive, as transport costs are a major component in their profitability. In 2019, Mongolian exporters expanded exports by 3 Mt (+11%), driven by increased demand in China.

Met coal exports in 2019 from the United States declined by 6 Mt (-10%), below 2017 levels, as import demand from Europe and Brazil was weak. Demand from Brazil, the largest importer of US coking coal, declined in 2019 as three major blast furnaces were undergoing maintenance.

Even with weak demand, Russia increased exports to Europe by 2 Mt, at the expense of the United States and Canada. On the other hand, exports to Korea and to Ukraine were weak, leaving Russia with a decline in exports of 2 Mt (-4.5%) in 2019.

Australia dominates met coal trade

Main trade flows in the metallurgical coal market, 2019 (Mt)

Open

{kind=link}

Metallurgical coal trade was dented in 2020, but will rebound with economic recovery

Global met coal imports are expected to decline by 29 Mt (-8%) in 2020. In 2021 a recovery of import volumes by 19 Mt (+6%) is forecast.

In 2020, Covid-related lockdowns and struggling economies dented steel production in virtually every country other than China, with direct impact on met coal trade. In the first-half of 2020 an increase in met coal imports to China occurred. The outbreak of the Covid-19 virus in China in the first-quarter reduced domestic supplies, as the reopening of many domestic coal mines was delayed from the beginning of February until March. However, imports in China are expected to decline in the second-half of 2020 because import restrictions have been tightened and import quotas are taking effect. For 2020 as a whole, imports in China are expected to remain roughly at 2019 levels, a trend which will continue through 2021, subject to changes in import policy.

Pig iron and steel production in India were severely impacted by Covid-related shutdown measures. India’s met coal imports are expected to decline by 10 Mt (-17%) in 2020, though met coal imports are projected to pick up by 7 Mt (+13 %) in 2021.

Similarly, in Japan and Korea steel production and thus the demand for met coal slumped sharply in 2020. It is estimated that Japan's met coal imports will fall by 9 Mt (-20%) in 2020. For Korea a decrease of 3 Mt (-8%) is estimated.

Recovery of the steel industry in Japan and Korea in 2021 is expected to be slow. Therefore, only a limited recovery in import volumes for met coal is expected: 3 Mt (+9%) in Japan and 1 Mt (+2.9%) in Korea.

Pig iron and steel production in Europe experienced a significant decline related to pandemic measures and subsequent economic turmoil. As a result, we estimate a decrease in met coal imports by 6 Mt (-11%) in 2020. For 2021 it is assumed that the industry will recover and met coal imports will increase by the same amount.

Metallurgical coal exports hit by the pandemic, but Australia recovers in 2021

Met coal exports are estimated to fall by around 43 Mt (-12%) in 2020, mostly seaborne traded met coal (-39 Mt). The decline in exports is more severe than the decline in imports, because the delay in discharging coal ships in Chinese ports at the end of 2019 meant that exports from the previous year could not be booked as imports until 2020. In 2021 a recovery in exports by 23 Mt (+7%) is projected. The share of seaborne traded met coal remains at 88%.

In the first-half of 2020, Australia was the largest exporter of met coal to China, which increased over 65% from the previous year. This notable increase was driven by the rebound of the steel industry in China and the temporary closure of its border with Mongolia, which hindered exports of its met coal. This border closure was suspended in the second-half of the year, so Mongolia is ramping up exports at the expense of Australia. Furthermore, exports to other major markets for Australian coal, e.g. Japan and Korea, are declining in 2020, leaving Australia with a fall in exports of 16 Mt (-9%). Recovery in 2021 will depend on China accepting Australian coal and could be challenged if the La Niña event impacts Australia’s coal supply chain.

The second-largest absolute decline in met coal exports, 13 Mt (‑26%), in 2020 is expected for the United States due to lower demand in key US markets such as Brazil and Europe. Exports to India are also expected to decline sharply. As US coal mines are confronted with relatively high cost structures, no recovery of exports in 2021 is projected.

Met coal exports from Mongolia declined by 5 Mt (-16%) in 2020, mainly due to temporary border closures with China. However, exports were above 2018 levels. We expect a rebound of 4 Mt (+14%) in 2021, assuming exports to China are not disrupted. On 1 January 2021, Chinese tariffs for Mongolian coking coal will go down to 1.5% from the current 3% level. This can benefit Mongolian exports, but a bigger boost will be the start of the 30 Mtpa capacity railway from Tavan Tolgoi to the Chinese border, scheduled to be operational by the end of 2021.

References

The volumes of annual imports and exports are different, as some exports reported in December are reported as imports in January. Trade volumes in this section refer to exports.

From 1 January 2020 the global upper limit of the sulphur content of ships' fuel oil was reduced to 0.50% (from 3.50%) by the International Maritime Organization (IMO). The reduced limit is mandatory for all ships operating outside certain designated Emission Control Areas, where the limit is already 0.10%.

Reference 1

The volumes of annual imports and exports are different, as some exports reported in December are reported as imports in January. Trade volumes in this section refer to exports.

Reference 2

From 1 January 2020 the global upper limit of the sulphur content of ships' fuel oil was reduced to 0.50% (from 3.50%) by the International Maritime Organization (IMO). The reduced limit is mandatory for all ships operating outside certain designated Emission Control Areas, where the limit is already 0.10%.