Cite report

IEA (2020), Sustainable Bioenergy for Georgia: A Roadmap, IEA, Paris https://www.iea.org/reports/sustainable-bioenergy-for-georgia-a-roadmap, Licence: CC BY 4.0

Report options

A bioenergy roadmap for Georgia

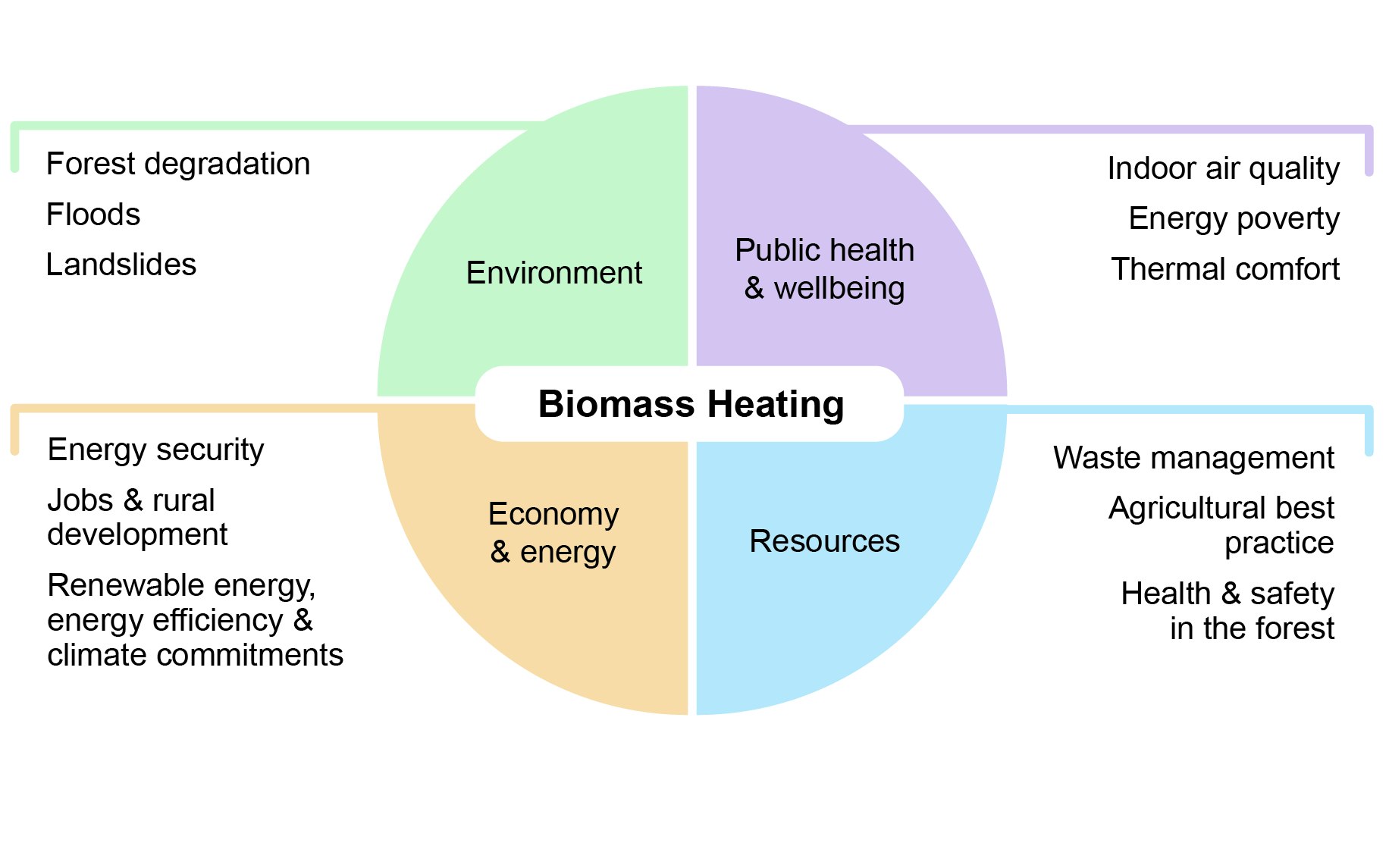

Biomass use in Georgia has implications not only for the energy sector, but far beyond. As the principal fuel used for household heating in rural areas, biomass is an important part of Georgia’s energy system. There is considerable scope to improve biomass supply sustainability and the efficiency of its consumption through better heating and cooking appliances, and to develop a modern bioenergy industry based on upgraded biomass fuels produced from diverse waste and residue feedstocks and potentially energy crops.

These developments would help counteract the negative impacts of the current unsustainable use of Georgia’s forestry resources, as well as facilitate modern bioenergy applications to support some of Georgia’s economic, environmental and social goals. These include:

- Improving energy security by maximising consumption of domestic energy resources rather than increasing reliance on imported natural gas and other fossil fuels.

- Ensuring the sustainable use of natural forest resources and the integrity of the natural environment and reducing the risk of natural disasters such as floods and landslides.

- Expanding formalised employment in biomass fuel supply in rural areas.

- Reducing the health impacts of indoor air pollution.

Wider considerations associated with biomass heating in Georgia

Open

{kind=link}

Fundamentally changing current practices in biomass supply and consumption is complex and requires a co-ordinated effort across government ministries and departments, the private sector and international development agencies. A more comprehensive set of policies, support schemes and regulations will be required to establish a modern bioenergy industry. For this reason, the government of Georgia should consider packaging the range of actions needed to modernise the use of biomass resources into a dedicated bioenergy strategy.

To facilitate the development of such a strategy, this roadmap focuses on:

- Ensuring biomass supply sustainability

- Modernising the consumption of biomass fuels.

For each of these points, the following sections offer examples of international best practices and suggested polices for Georgia’s current context.

However, while improvements in these two areas are important, these alone will not be sufficient to remedy the environmental issues associated with the management of Georgia’s forestry resources, or social problems such as fuel poverty and indoor air pollution. This will also require comprehensive action in a number of areas outside the scope of this roadmap, such as raising the energy efficiency of the housing stock and supporting the installation of a wider range of sustainable heating systems such as solar thermal panels and heat pumps.

It may also be necessary to evaluate the extent to which public investments affect the achievement of sustainability goals. Other areas that warrant further assessment are fossil fuel subsidisation (e.g. related to natural gas infrastructure and consumption) and policies related to waste management.

Ensuring biomass supply sustainability

Employing best-practice forestry management can ensure biomass fuel supplies while avoiding deforestation and its associated environmental impacts. Furthermore, using waste and residues can diversify the types of biomass used as heating fuels and reduce pressure on Georgia’s forestry resources, while also providing rural job creation opportunities and an avenue for managing municipal, agricultural and forestry wastes and residues. The principal objective of this section’s recommendations is not necessarily to raise bioenergy use from the current level, but to replace firewood with a diverse set of other fuels from sustainable feedstocks.

Georgian context

This section provides an overview of the different biomass resources available in Georgia.

Forestry management and forest residues

There is considerable scope to improve the management of Georgia’s forests, and the production of sustainable biomass fuels.

An update to Georgia’s Forest Code was approved by parliament in May 2020 and will come into force in 2021. The updated code creates a legal basis for sustainable forestry management processes and will strengthen the state’s capacity to supervise and detect illegal forest activity. Clearcutting of forests is prohibited in Georgia.

Georgia’s current “social cutting” policy allows the population to source a designated volume of fuelwood from the forest. Under this policy, the Forestry Agency determines annual quotas and marks trees that can legally be cut. However, this policy and the wider issue of illegal firewood harvesting is problematic for many reasons:

- Unqualified people with inadequate equipment often carry out firewood sourcing. This damages the forest ecosystem, and a lack of supervision heightens the risk of accidents.

- Black market activity deprives the state of revenue and diverts timber suitable for higher-value uses (e.g. wood products) to lower-value energy production.

- Illegal firewood sourcing commonly overlooks trees in remote or difficult-access areas permitted for felling under the social-cutting quota, in favour of more accessible trees in already degraded areas around towns and villages that present lower logistical challenges and costs.

- Illegal fuelwood sourcing leaves a significant portion of forestry residues in the forest, which:

- increases the risk of forest fires, to which 400 000 ha of Georgia’s forested area is vulnerable, as well as insect infestations

- prevents forestry residues from being upgraded to heating fuels such as woodchips, wood pellets or briquettes that are suitable for modern heating appliances.

- It hinders the market prospects of more sustainable fuels, as the extra collection and processing costs for wastes and residues cannot compete with low-cost unsustainably sourced logwood.

The updated Forest Code proposes abolishing the social-cutting system by 2023 – a key step to resolve some of the issues outlined above. Nevertheless, given citizens’ reliance on fuelwood for residential heating and cooking, affordable alternative heating fuels must be made available to reduce fuel poverty and maintain social stability.

One solution is to maximise the use of available forestry residues, such as those that have accumulated in forests after illegal forest harvesting and those arising from environmental events, as well as biomass made available through forest management practices not currently being undertaken, e.g. from thinning and the removal of bush species to promote new forest growth.

Residue recuperation could provide around 8 PJ of material annually to produce upgraded biomass fuels (WEG, 2014) – more initially, as these unexploited resources have accumulated over time. However, as this assessment includes residues arising from illegal forest activities, their successful phaseout could reduce this energy potential by approximately half.

Challenges associated with using these forestry residues include collection costs given the difficult terrain in many areas, logistics because of limited road networks in some areas, and the lengthy time required for residues to dry to a suitable energy content for upgrading.

The revised Forest Code should reduce the supply of fuelwood and correspondingly increase its cost, thereby improving the relative economic case of more sustainable upgraded fuels. Nevertheless, supportive measures are still required to establish a forestry residue conversion business case that will be attractive to the private sector.

The updated Forest Code also proposes that the Forestry Agency provide biomass fuels at forest borders. The details of how this will be undertaken are still in development, with the creation of a public body to oversee these activities a potential option. Several business/supply yards have already been constructed for this purpose, and their number is planned to increase to over 50 by the end of 2021. Although this is encouraging, the scale of fuelwood consumption in the country may require even more facilities. These facilities could also serve as centres for forestry residue collection.

The price of residues is currently similar to the social-cutting licence fee, which is likely to make the use of forestry residues for fuel production uncompetitive. Selling forestry residues through an auction system is therefore under consideration.

Sawmills are a prime source of biomass supplies for the manufacture of upgraded fuels. They produce easily collectable sawdust, a feedstock that can be used for biomass briquettes and pellets. Sawdust from Georgia’s sawmills is largely unused, and annual production potential has been assessed at 0.3 PJ (WEG, 2014).

Furthermore, sawdust has accumulated over the years due to a lack of legal disposal options for sawmills, although illegal burning and dumping into rivers has also occurred, causing negative environmental impacts to the air and water. Facilitating the use of sawdust will require the development of localised solutions for supply logistics, drying (as sawdust initially has a high moisture content) and upgrading.

Agricultural wastes and residues

Agriculture is a key sector of Georgia’s economy and provides employment for more than half the population. Around 35% of the country’s territory is agricultural land, of which 30% is for perennial crops and the rest is sown annually. The country practises mainly subsistence agriculture, and it is therefore fragmentary, with more than 90% of agricultural output from small-scale family-run farms and smallholdings.

Crops produce biomass residues that can serve as feedstock for briquettes and pellets. Upgrading these residues to fuels is important: first, it increases the energy density of the material (i.e. energy per m3) allowing for more economical transport over longer distances; and second, it makes the crop residues suitable for more efficient use in modern heating appliances.

Crop residues come from several sources:

- Perennial crops: vine pruning and pressing residues; fruit orchard pruning and pressing residues; hazelnut shells; walnut shells; and bay leaf residues.

- Annual crops: corn, wheat and barley straw; and sunflower residues.

Analysis indicates these residues have a theoretical energy content of 28 PJ, and an achievable energy content of roughly 7.7 PJ (WEG, 2014). Some of these residues are already used for non-energy purposes, however (e.g. straw for animal bedding).

Deliverable potential of agricultural residues in Georgia

OpenAlthough some agricultural residues are already used for energy, it is generally in isolated and informal cases. There are examples of bay leaf and vineyard residue use for agroindustrial heating and drying purposes, and in the Samegrelo and Guria regions it has been shown that with minimal adaptions, boilers and stoves can use hazelnut shells directly.

Overall, however, very little agricultural residue potential has been realised because of collection and logistics challenges that make it difficult to ensure reliable fuel supplies.

Residues are produced seasonally: for example, waste biomass is available from spring to autumn while heating fuel demand is highest in the autumn and winter, requiring fuel storage and raising costs. In addition, the bulkiness of many agricultural residues means transport over distances of more than 50 km (and sometimes less) is uneconomical, making it more logical to favour local use or upgrade to increase fuel energy density.

Consequently, agricultural residues either remain uncollected or in some cases are burned in the field (e.g. wheat straw and vine trimmings). Not only does this not valorise their fuel potential, it produces particulate matter emissions that deteriorate air quality. Field burning can also unintentionally destroy windbreak trees, which is detrimental as the soil in many parts of Georgia is susceptible to wind erosion.

Wine production in Georgia is expanding rapidly. Vine trimmings are produced seasonally, usually during the three-month spring period, and there is no industry standard for their sustainable disposal. They are commonly burnt, as transportation and storage costs outweigh their value for fuel production in the current market context. If this dynamic were to change, vine-pruning residues could be converted to heating fuels through baling, drying and size-reduction processes (e.g. shredding). Following this they could also be upgraded to pellets.

There is potential for wine producers to either produce fuels or, to avoid the trimming, collection and disposal costs that would otherwise be borne by the winery, enter into a mutually beneficial relationship with fuel producers to take trimmings for fuel production.

Costs can be around GEL 100/ha (USD 30/ha) for trimming and collection, with additional disposal costs. In 2020, a project was initiated in the Telavi municipality to test equipment for collecting and processing vine clippings, with the goal of providing heating fuel for two municipal kindergartens.

Aside from difficulties in establishing supply chains, further challenges need to be overcome to accelerate the development of agricultural residue-based fuels so that they can make a notable contribution to the biomass fuel market:

- Price escalation from suppliers once they realise there is a market for previously unused residues.

- Agricultural residues are not covered under waste management legislation, so producers are not obligated to collect and use them sustainably.

- A universal value-added tax (VAT) of 18% is applied to all fuels, with no distinction between fossil and renewable.

- High capital costs for small-scale producers to invest in the equipment necessary to upgrade residues to fuels.

Banks do not offer producers low-interest credit to purchase fuel upgrading equipment, leaving them with limited alternatives to taking out regular loans at high interest rates, commonly >10%.

Energy crop plantations

Energy crops can further diversify the supply of biomass fuels, and Georgia appears to have favourable climatic conditions for the cultivation of certain species, notably poplar, which grows well on poor-quality (e.g. high-moisture-content) land unsuitable for food crops, and alder species. A decline in Georgia’s agricultural output has increased the share of unused agricultural land to roughly 130 000 ha (40% of all arable land) (World Bank, 2015).

Poplar plantations could provide feedstock for fuel briquette production (one has already been established in western Georgia). One plantation developer has indicated a calorific value for poplar of around 15 megajoules per kilogramme (MJ/kg), equal to fuel costs of around GEL 28 per gigajoule (/GJ) (USD 8.5/GJ). Poplar can offer a heating value of up to 20 MJ/kg, however, which would reduce fuel costs in energy terms.

Nevertheless, as other non-energy uses for poplar exist (e.g. for furniture and windbreaks1), plantation owners would need to assess which markets offer the highest returns, meaning that plantations may not always be used to produce fuel once established.

Poplar trees (© Marani JSC).

Another potential benefit of energy crop plantations is rural job creation, as people are required for planting, maintenance and harvesting, as well as for fuel production. The number of jobs (e.g. jobs per hectare of land) will fluctuate over a plantation’s lifetime, however, with most employment opportunities arising in the planting and harvesting phases.

International experience shows that developing markets for energy crop production can be difficult. From a production standpoint, securing investments to establish plantations is challenging because an initial investment is required to purchase and clear the land and plant the crop, and the subsequent delay before any revenues are realised is long (for poplar trees, the first harvest could be five years after planting). Some economic support from the government and offtake commitments for fuel are therefore likely to be needed to kick-start plantations. The GEDF has received one application for an energy crop plantation project.

Municipal waste

Georgia has over 60 registered landfills, around 30 unofficial ones in villages without formalised waste management services, and numerous illegal dumping areas. There is considerable scope to modernise waste management and reduce associated environmental impacts to land, water and air, and the release of methane2 from waste disposal. With donor and international financial institution (IFI) support, old landfills are being closed and remediated, and new landfills compliant with EU requirements are being constructed.

A modernised waste management sector would also include EfW plants. There are currently no EfW plants in Georgia and no landfill gas production, and municipal waste is not segregated to produce refuse-derived fuel (RDF). Urban green waste also goes into landfills.

The 2014 Waste Management Code:

- Stipulates that waste segregation should begin in 2020.

- Prohibits the burning of waste other than in permitted incinerators.

- Requires that municipalities prepare waste management plans.

- Calls for a strategy with concrete targets and measures to reduce the landfilling of biogenic waste.

Implementing these requirements has proved challenging so far. While many municipalities are integrating provisions from municipal waste management plans, actual progress (e.g. to improve waste separation) is currently limited. However, as successfully meeting these targets will enhance the quality of waste management and facilitate EfW project development, Georgia has adopted a National Waste Management Strategy for 2016-30 to guide implementation.

Unfortunately, Article 2 of the Waste Management Code specifically excludes non-municipal biomass materials, e.g. agricultural/forestry residues and sewage. This permits informal biomass residue utilisation and is not conducive to best-practice use of these resources.

International best practice in biomass supply

Sustainable forest management in Sweden

In Sweden, bioenergy plays a central role in all aspects of the energy system. Bioenergy accounted for one-fifth of the country’s final energy consumption in 2017, and more than half of all space heating in the housing and services sectors (Svebio, 2020).

Sweden’s solid biomass supply is highly sustainable: despite a near-doubling of solid biomass in primary energy supply since 1990, forest stock (i.e. the volume of living wood) has increased 23% through sustainable forestry management, with growth exceeding felling.

Forest standing stock, growth and felling in Sweden, 1990-2016

OpenSwedish forest law considers that all forests with a growth rate of more than one cubic metre per year are productively managed forests. Over 60% of productive forest land is certified, mostly through the Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC) schemes.

Around 70% of forest wood growth is felled each year, and the remainder is untouched, providing ongoing carbon uptake. All elements of harvested trees are used, with the highest-value material used for lumber, pulp and paper products, and other wood products. Higher-value stemwood is generally not used for energy, with the exception of small trees removed from forest management operations (e.g. through clearing and thinning), or when it has been discarded and cannot be used for industrial purposes.

Biomass for energy use is integrated into the Swedish approach. Biomass fuels are produced from wood-processing residues from the abovementioned industries (e.g. bark, shavings and wood chips) and from felling residues (e.g. branches and tops) that are unsuitable for industrial use. Less than 10% of all harvested material (by energy content) is used for bioenergy production.

Harvested areas are replanted, with this form of active management leading to higher growth than in mature forests and therefore greater CO2 uptake. Furthermore, sustainably managed forests are more resistant to forest fires and infestations, reducing the risk of significant CO2 release that can result from such events.

Agricultural residues

Denmark is also a leader in bioenergy. Biomass makes up over one-fifth of primary energy supply, and over half of all fuel used for district heating. Since Denmark does not have notable forest resources, in addition to importing biomass fuels it has developed the technology to use domestic straw residues from agriculture.

Straw boiler plant (© AffaldVarme Aarhus)

Such modern systems can achieve efficiencies of over 90% but require specialised strawbale feeding mechanisms and tightly controlled combustion temperatures to manage air pollutant emissions (e.g. from fly ash) and avoid technical problems such as slagging that arise when ash melts inside the boiler.

Europe possessed around 45% of global vineyard area in 2015 (Karampinis, 2020), with the majority in France, Italy and Spain. The production of biomass fuels from harvesting residues is not widespread, although there have been some trials and successful examples of small-scale commercial production from fuels used on-site or supplied locally.

Experience indicates that careful planning is required if vineyard residues are to be used for energy purposes. Initial assessments should comprise 1) an evaluation of local conditions (e.g. biomass productivity [tonnes/ha]) and identification of end uses; 2) a selection of appropriate harvesting methods and equipment; and 3) confirmation that combustion equipment is suitable (Karampinis, 2020).

Harvesting equipment also needs to be appropriate to ensure suitable characteristics (e.g. chip size) and – crucially – to avoid introducing contaminants such as soil and stones. For this reason, mechanical systems that avoid soil lifting are preferable. Where average landholdings are small, co-operative business models are likely to be most favoured. After harvest, a drying period will probably be required to reduce moisture content.

Because the low energy density and form of vine cuttings impede direct utilisation in smallscale combustion systems, initiatives in Europe have focused on energy densification through pelletisation. As vine prunings generally have a lower fuel quality than woody biomass, with higher ash, nitrogen and potassium content, sophisticated feeding and combustion systems and/or appropriate biomass cleaning are needed prior to pelletisation.

Energy from waste (EfW)

Energy recovery from municipal wastes offers multiple benefits compared with landfill disposal, as indicated by its higher position in the waste management hierarchy.3 EfW facilities reduce waste volumes significantly and require less land area than landfill sites.

From a sanitary and environmental perspective, compared with landfilling, energy recovery reduces odours, GHG emissions, and emissions to the groundwater and soil. EfW technology also offers electricity and heat close to the point of demand using locally available resources, which diversifies the local energy supply.

Waste disposal costs and share of EfW in selected countries

OpenIn the European Union, almost 30% of waste (by volume) produced in 2017 was used to produce energy. However, several countries achieved higher shares, with four over 50%: Denmark, Sweden, Finland and Norway. There is a close correlation between waste disposal costs and EfW deployment, as all four countries have landfill taxes and certain forms of landfill bans, e.g. for organic material.

EfW projects can be highly sustainable. In the Netherlands, for example, the city of Utrecht has a 30-megawatt thermal (MWth) biomass plant that provides heat to 50 000 households and businesses through a district heating system. The plant uses biomass fuels produced from green waste from the maintenance of parks, public gardens and forests in the region.

Key policies for biomass supply sustainability

Key overarching actions

- Actively implement the updated Forest Code drawn from best-practice sustainable forestry management principles (e.g. of the FSC and PFEC) adapted to the Georgian context.

- Promote an appropriate transition away from the social-cutting policy, with measures that ensure affordable and sustainable alternatives to fuelwood to avoid increasing fuel poverty.

- Establish a regulatory framework for the collection and disposal of commonly produced agricultural residues, which prohibits in-field burning and facilitates sustainable energy uses.

- Formally adopt a strategy for the production of upgraded biomass fuels such as pellets, woodchips and briquettes, identifying key steps to develop self-sustaining businesses. Such a strategy was produced with support from UNDP but is yet to be approved.

- With international donor support and using best-practice examples, enact replicable sustainable biomass fuel and waste management pilots to identify those with most promise.

Specific policies and actions for consideration

Forestry:

- Expand the number of Forestry Agency business yards (for forestry residue collection depots) and potentially as locations for fuel upgrading, with equipment purchased through PPPs or co-operatives.

- Consider transferring some current harvesting and fuelwood jobs in rural areas to a sustainable biomass industry.

Agricultural residues:

- Obtain international donor assistance to aid ‘technology leapfrogging’ to the most appropriate equipment and processes to combust straw and other agricultural residues.

Energy crop plantations:

- Support the establishment of a ‘showcase’ energy crop planation, with the aim of guaranteeing a future offtake of fuel produced for public sector heating demand.

Wastes:

- Adopt policies to increase the cost of (or prohibit) landfill waste disposal, such as banning the landfilling of certain materials or imposing landfill taxes, to encourage higher-value end uses, including EfW processing.

- Enact the collection of urban green wastes and source segregation of municipal solid waste (MSW) to improve waste management and boost supplies for fuel production.

- Assess the amount of waste and residue feedstock available for biogas production and determine the contribution biomethane could make to natural gas supplies.

- Develop a regulatory framework that covers biomass waste and residues and requires disposal routes in keeping with the waste management hierarchy (including energy recovery).

Modernising biomass consumption

The single most effective measure to improve the sustainability of biomass use in Georgia is to transition to more efficient heating appliances. Using more sophisticated biomass heating systems that combust upgraded fuels has multiple benefits. First, replacing the basic systems used for biomass combustion with improved heating appliances would offer more controlled and complete combustion, which, coupled with adequate ventilation (e.g. a flue), would reduce indoor air pollution and consequential health impacts. Thermal comfort and automation would also be improved.

Second, higher-efficiency modern systems using upgraded fuels means less fuel for the same heat output, reducing pressure on Georgia’s fuel supply and forestry resources.

Furthermore, programmes to install improved biomass heating systems and develop supply chains for upgraded fuels create skilled jobs, e.g. in system installation and maintenance, fuel upgrading and logistics.

Georgian context

This section outlines the heating appliances and types of biomass fuels used in Georgia.

Heating systems and appliances

Basic firewood heating stoves are commonly used. They generally have a low efficiency of 25-35% (GIZ, 2019), although stove efficiency is not verified through testing. Their design is simple, with no mechanism to control air inflow, and they are not airtight. Consequently, combustion is uncontrolled and occurs quickly at high temperatures, and the lifespan of basic stoves is relatively short at around five years. Open fires, which are even less efficient, are also commonplace.

Combustion efficiency is hindered by many households using wet firewood to slow the pace of combustion. In a residential context, it is advisable that solid biomass fuels not have a moisture content >25%, as higher moisture levels reduce the combustion temperature and result in greater smoke formation and health-damaging particulate matter emissions.

Typical emissions factors for various biomass heating devices

|

Biomass heating device |

PM (g/GJ) |

% organic carbon |

|---|---|---|

|

Open fireplace |

322 - 1 610 |

40 - 75% |

|

Simple log stove |

140 - 225 |

50% |

|

Modern log stove |

46 - 90 |

20% |

|

Pellet stove |

3 - 43 |

10% |

|

Pellet boiler |

3 - 29 |

5% |

|

Biomass boiler without emissions control |

28 - 57 |

3% |

|

Biomass boiler with emissions control |

8 - 15 |

2% |

Note: g/GJ = grammes per gigajoule. Sources: Koppejan and de Bree (2018), Kennisdocument Houtstook in Nederland [Knowledge Document in the Netherlands]; Vincente and Alves (2018), “An overview of particulate emissions from residential biomass combustion”.

In Georgia, fuelwood generally has moisture content well in excess of 25%, and up to twice as high. Drying wood from 40% to 25% moisture content can increase its energy content by around 40%,4 but requires air-drying for several months in dry conditions. Drying equipment can reduce moisture content far more quickly but entails additional cost.

The single most effective measure to improve the sustainability of biomass use in Georgia is to transition to more efficient heating appliances. Changing to more modern heating stoves and boilers is required for two key reasons: first, to increase the efficiency of fuel combustion; and second, to facilitate the use of drier wood fuels and (preferably) upgraded fuels produced from a diverse set of biomass feedstocks. Both would reduce pressure on Georgia’s forestry resources from residential heat demand.

Improved wood stoves with combustion chambers and air inlet controls are produced domestically on a small scale and in a nonstandard manner. They are likely to be more efficient than basic stoves, but the extent of their efficiency has not been fully quantified due to a lack of testing programmes. Nevertheless, an improved Svanetian stove with 45% efficiency can reduce firewood consumption by around one-third compared with a 25%-efficient appliance, while a stove with 75% efficiency would cut firewood consumption by two-thirds compared with the basic alternative. In both cases, using a more efficient stove considerably reduces the cost of delivered heat for a household.

As the energy efficiency performance of stoves varies significantly from one model to another, standardisation, which in turn permits certification (e.g. of energy efficiency performance) is crucial to promote domestic stove manufacturing. In Akhmeta, GIZ is undertaking a programme to foster the development of alternative, energy-efficient and renewable energy sources, which will focus on testing, standardising and certifying energy- efficient stoves.

Domestically produced wood stoves cost GEL 300-550 (USD 95-175), equating to (at the upper limit of the price range) half of a rural Georgian household’s average monthly income in 2019. Despite the higher purchase cost, an improved stove can pay for itself quickly (i.e. in less than one year) thanks to its higher efficiency.5 However, the general population is largely unaware of the benefits of improved heating appliances.

Although better-quality imported household stoves are available on the market, their higher capital costs mean they are generally not an economically viable alternative for most households without innovative support measures or financing schemes. There is also a lack of suitably trained system specifiers, heating engineers, installers, etc., and turnkey solutions are uncommon.

Most current initiatives using improved heating systems are feasibility studies or one-off pilot projects. Some pilot projects in public buildings have used imported “best-in-class” biomass boilers that offer high levels of efficiency and automation, but their long-term use requires a reliable supply of suitable fuel and qualified maintenance engineers, which can be challenging to find in Georgia. The high quality of such systems also means elevated capital costs, so these projects are often not replicable without financial support. More widespread deployment would therefore require ongoing development financing.

Upgraded fuels

While the use of fuelwood is culturally ingrained, the consumption of other forms of biomass fuel is not. As awareness of biomass pellets, briquettes and other upgraded biofuels is low, their use remains very limited.

Briquettes have favourable combustion characteristics compared with fuelwood: higher calorific value owing to their lower moisture content, and higher density. Consequently, they burn for longer at more uniform temperatures and more efficiently, offering greater thermal comfort.

The market for briquettes is relatively undeveloped, but there are early signs of growth. In 2019, around 15 000 m3 of firewood demand was replaced with briquettes. Domestic production is estimated in the range of 5 000 to 7 000 tonnes per year, equivalent to roughly 1% of all biomass fuel (by energy value) used in Georgia. Production is from small companies, and key supply-side market challenges are to mobilise feedstock supplies (e.g. sawdust or hazelnut shells) and to access capital to invest in production equipment. There have been instances in which production growth has been constrained by local feedstock availability or feedstock price escalation.

The main briquette consumers are public bodies (e.g. schools and municipal buildings), as general consumer awareness remains low, with most new customers learning of the fuel through word of mouth. In some case, briquettes have had to be provided free of charge for a period to demonstrate their additional value over fuelwood. Supplying end users over great distances is generally uneconomic, ruling out markets far from production sites that are located based on feedstock availability. Meeting household demand is also problematic due to low purchase volumes and the lack of retail outlet suppliers. The approximate cost of briquettes delivered to end users is around GEL 500/tonne.

Although public procurement could help boost supplies and support early-stage market development for upgraded fuels, procurement practices have instead hindered market access for some independent fuel suppliers. This has occurred where state procurement guidelines have specified that public buildings may purchase logwood only or must source the least costly (and not necessarily the best) fuel. Many tenders specifically request firewood or are based on volume rather than heat content, as municipal governments lack the heating expertise necessary to make informed fuel supply decisions. Furthermore, some public institutions do not pay for heat, so have no incentive to maximise efficiency.

General obstacles to market development for all types of upgraded biomass fuels include:

- Low and, in the case of illegal consumption, zero-cost unsustainable firewood supplies.

- A lack of consumer awareness regarding upgraded fuels, and unfamiliarity with the concept of purchasing fuels or heat energy in many areas.

- Challenges in establishing reliable supply chains for feedstocks and upgraded-fuel distribution.

- High interest rates for entrepreneurial fuel producers seeking the capital necessary to purchase equipment to expand operations.

- Absence of supportive policies and financial mechanisms for production and consumption.

- Incompatibility with the basic stove types commonly used in rural areas.

Other initiatives to produce modern biomass fuels and take advantage of the variety of untapped resources available in Georgia are not widespread. Only a limited number of cases use agricultural residues for energy, mostly linked to processing industries. A number of isolated biogas pilot projects have also been initiated; for example, the European Investment Bank has supported upgrading of Kutaisi’s municipal water sector infrastructure, which will involve biogas production. Generating thermal energy from waste (e.g. through co-generation) is not utilised.

Stove and fuel economic analysis

An economic analysis of the cost of fuelwood and briquettes used in appliances of different efficiencies has been conducted to aid decision-making. Key findings are outlined below.

Fuel and delivered heat costs

|

Fuel |

Fuel cost range (GEL/GJ) |

Stove type and combustion efficiency |

Reference stove capital cost (GEL) |

Delivered heat cost range (GEL/kWh) |

|---|---|---|---|---|

|

Firewood |

13-18

|

Basic, 25% |

60 |

0.18 – 0.26 |

|

Firewood |

Improved, 45% |

300 |

0.10 – 0.15 |

|

|

Firewood |

Efficient, 75% |

500 |

0.06 – 0.09 |

|

|

Briquettes |

23 - 32

|

Basic, 25%* |

60 |

0.24 – 0.33 |

|

Briquettes |

Improved, 45% |

300 |

0.19 – 0.26 |

|

|

Briquettes |

Efficient, 75% |

500 |

0.11 – 0.16 |

|

|

Natural gas |

16 - 17 |

Boiler, 90% |

1 500 - 3 000 |

≈ 0.06 |

* Using briquettes in basic stoves is not recommended for safety reasons. Notes: kWh = kilowatt hour. Moisture content of firewood: 40%; briquettes: 12%. Lower calorific value of firewood: 10 MJ/kg; briquettes: 17 MJ/kg. Natural gas boiler costs do not include the cost of internal heat distribution pipework and radiators. Source: Eurostat (2020a), Gas Prices for Household Consumers (database), https://ec.europa.eu/eurostat/data/database.

Fuel costs for firewood are lower than for briquettes; however, the cost of delivered heat from briquettes used in an improved stove is broadly similar to firewood in a basic stove – plus they offer greater thermal comfort, lower air pollutant emissions and reduced pressure on forestry resources. The cost of delivered heat using briquettes in an efficient stove is lower than for firewood in a basic stove.

Using briquettes in basic stoves is not advisable due to the combination of their high combustion temperature and the thin lining of basic stoves, creating potential for injury. It should also be noted that using briquettes in simple stoves can shorten the appliance’s lifespan due to their high burning temperature. Basic stoves are also not suitable for other upgraded fuels such as pellets or wood chips, creating a market barrier for these fuels.

Annual fuel costs for an average household with heat demand of 4 000 kWh per year (equivalent to 11 m3 of firewood) would therefore be roughly the same for firewood in a basic stove and briquettes in an improved stove, with both in the range of GEL 750-1050/year (USD 230-325/year). Annual fuel costs of using briquettes in an efficient stove would be lower, at GEL 450-620/year (USD 140-193/year).

Compared with the upper-limit cost of using firewood in a basic low-efficiency stove, the energy savings offered by using low-cost briquettes in an improved stove would easily pay for the additional cost of the appliance in less than one year. Assuming mid-range fuel costs for using firewood in a basic stove, the extra investment for an efficient stove using briquettes could be paid back in 12-18 months.

Georgia’s household natural gas costs, which are subsidised, were the lowest in Europe in 2019, at around one-quarter the average EU residential gas price. Household gas prices were also one-third lower than commercial rates in 2019. These artificially low gas prices, combined with the high efficiency of modern gas boilers, offer more delivered heat per cost than unsubsidised briquettes and even fuelwood – even in the most efficient stoves.

However, several factors must be considered:

- The prohibitive capital cost (for many households) of a modern natural gas boiler, as well as further heat distribution pipework and home radiator expenses

- The cost to the state of subsiding natural gas prices on a per-unit basis and the extension of natural gas transport infrastructure to rural areas

- Energy security implications, as natural gas is almost entirely imported.

The current very low gas prices as a result of the COVID-19 crisis offer the Georgian government an opportunity to reassess fossil fuel subsidies.

International best practice in biomass consumption

The following examples of good international practices can help guide the development of sustainable biomass consumption in Georgia.

Residential wood pellet markets in Austria and Italy

Residential and commercial heating accounts for over half of all wood pellet consumption in the European Union. Austria and Italy are two of the major residential wood pellet markets.

In Italy, biomass provided around one-fifth of residential heat demand in 2018. Around 9% of households have a pellet stove, equating to 2.4 million installations and 3 million tonnes (Mt) of wood pellet consumption in 2018, by far the largest domestic market globally.

In Austria, biomass met close to 30% of residential heating demand in 2018. Austria’s pellet stove market is smaller at around 50 000 units (1% of households), but installations are on an upward trend, expanding by two-thirds over 2010-18. Large-capacity biomass heating systems are more common in Austria. Around 3% of households own biomass boilers, and biomass district heating is also used.

New installations are commonly modern automated systems that offer around 90% efficiency and comply with air pollution regulations, thanks to combustion control to ensure optimal combustion temperatures and air-to-fuel ratios. Plus, certifiction ensures appliance quality: for example, in Italy, AriaPulita certifies domestic appliances and provides a star rating based on efficiency and emissions.

The pellets most commonly used in both countries meet the highest quality specifications (A1), having less ash content and therefore lower associated particulate matter emissions.

Wood pellet market overview in Austria and Italy, 2018

OpenAround 80% of feedstocks for pellet production in Italy are secondary residues from wood processing.

However, Italy also imports wood pellets because its demand exceeds national production capacity and feedstock availability. Additional supplies come mostly from neighbouring Austria, which has over three times Italy’s production capacity. All of Austria’s wood pellet production comes from secondary residues.

Policy has played a key role in promoting the use of residential biomass heating systems. In Italy, renewable heat installations are eligible for a tax reduction. Alternatively, the Conto Termico scheme provides two years of payments for households installing biomass systems of <35 kW capacity.

Financial support is contingent on the heating system meeting prescribed limits for particulate matter emissions, and households cannot receive both support measures for the same system.

In Austria, the Environmental assistance in Austria (UFI) programme provides purchase incentives for biomass and other renewable heating systems, of up to 35% of investment costs, but installations must meet certain quality standards to be eligible for support. Support levels are highest for the replacement of fossil-fuelled heating systems, with the next-highest support offered for replacing an old wood heating system (pre-2003) with a modern biomass heating system.

Austria also has a specialist training programme for installers of renewable heating technologies as well as guidelines for public buildings to set a good example, including by using renewable technologies as widely as possible.

Source: Bioenergy Europe (2019), Statistical Report 2019: Pellet Report.

EN Plus Wood pellet certification

EN Plus is an independent third-party scheme for wood pellet certification, covering around 12 Mt of supply across 46 countries in 2020. In 2018, 85% of pellets produced in the European Union were from forestry residues. The scheme ensures consistent fuel quality by assessing the entire fuel supply chain, and pellets meet established technical specifications (calorific value, ash content, size, durability, moisture content, etc.) largely based on the international ISO 17225 standard. This ensures that poor-quality or inappropriate fuels do not needlessly shorten the lifespan of heating appliances.

The Baltpool biomass exchange

This exchange facilitates the trading of biomass fuels in Lithuania (e.g. wood pellets and wood chips) by providing a platform that connects suppliers and purchasers. In 2019, over 95% of all purchases by regulated heat producers took place over the exchange. Sellers submit offers and specify the distance over which they are prepared to deliver, and the exchange matches purchasers with the best suitable offer. The exchange has increased transparency and the number of suppliers in the marketplace.

This increase in supply liquidly has in turn reduced biomass fuel prices and delivered greater uniformity of pricing. Furthermore, suppliers are validated to ensure they are technically and financially able to fill orders and that fuels supplied meet the established technical specifications, thereby raising purchaser confidence. Timber and forestry residue trading has also been included since 2018.

Heat mapping

Many countries and regions throughout Europe have undertaken heat-mapping exercises to produce geographic information system (GIS) visualisation tools to guide public sector decision makers and industries in the best-practice deployment of low-carbon heating solutions. These show the density and source of heat demand (e.g. industry, residential, public sector) in a geographic area and allow comparison with the availability of local supply sources (renewable energy sources, waste heat, etc.). This initial data collection exercise can also be used to create a baseline to monitor and assess the impacts of policies and measures. In the Georgian context, heat mapping could match sustainable biomass resources with heat demand, as well as inform the deployment of district heating systems and projects to produce upgraded biomass fuels.

Adjusted VAT rates

Several European countries apply a lower VAT rate for biomass fuels to incentivise a switch from fossil heating fuels such as natural gas, heating oil or coal to sustainable biomass.

General and biomass fuel VAT rates for selected countries, 2018

|

Country |

VAT rate for wood pellets (%) |

General VAT rate (%) |

|---|---|---|

|

Austria |

13% |

20% |

|

Belgium |

6% |

21% |

|

Germany |

7% |

19% |

|

France |

10% |

20% |

|

Lithuania |

9% |

21% |

|

United Kingdom |

5% |

20% |

Note: The United Kingdom has reduced the VAT for all domestic heating fuels. In the other countries listed, the VAT on biomass fuels is lower that for fossil heating fuels. Sources: Bioenergy Europe (2019), Statistical Report 2019: Pellet Report; EC (2019), VAT Rates Applied in the Member States of the European Union, https://ec.europa.eu/taxation_customs/sites/taxation/files/resources/documents/taxation/vat/how_vat_works/rates/vat_rates_en.pdf.

Key policies for modernising biomass consumption

Key overarching actions

- Harness donor funding and the capacity of the GEDF to support programmes (e.g. technical assistance to design projects, conduct feasibility assessments, secure grants or soft loans, purchase efficient stoves economically, and establish upgradedfuel supply businesses).

- Use donors’ technical assistance to improve national competences in: a) producing, installing and maintaining efficient stoves; and b) producing upgraded biomass fuels.

- Identify regional clusters of biomass supply and heat demand,6 and launch focused initiatives to establish upgraded-fuel production businesses in these areas.

- Establish a strategic communication strategy to enhance public awareness of the benefits of higher-efficiency heating appliances and upgraded fuels, best-practice combustion practices, and the health impacts of poor air quality.

Pilot project considerations

Using development funding to create biomass boiler and stove pilot projects is a means to highlight best practices and stimulate early-stage market development. However, while it may be tempting to use best-in-class technologies for pilot projects, these may ultimately be hard to sustain due to challenges in obtaining suitable fuels, maintenance expertise and parts. Furthermore, the high capital costs of the most sophisticated biomass boilers and stoves means that such projects are challenging to replicate.

Rather than conducting one-off projects, development funding for pilots would be more effectively used to install higher-efficiency stoves and boilers (e.g. with suitable air inlet controls), at capital costs that allow for the creation of local, self-sustaining business models. The production of these appliances should be standardised to permit performance and energy efficiency verification. Using part of the budget to offer co-funding of systems and institutional support for end users is also a means to ensure sustained success. As several pilot projects of this nature have already been undertaken, drawing on their experiences is a logical starting point for policy development.

Specific policies and actions for consideration

Supporting fuel supply businesses:

- Support new fuel production businesses through financial de-risking measures (e.g. grants, soft loans or fiscal measures) to facilitate investment in equipment.

- Create capacity-building and training opportunities to offer technical support to biomass fuel producers from industry leaders in briquette and pellet production.

- Establish an active industry association to support the common interests of biomass fuel businesses though the dissemination of information and lobbying on their behalf.

Optimising fuel procurement:

- Reform procurement guidelines and processes to ensure that sustainability is a key criterion in sourcing biomass heating fuels.

- Use public sector demand to stimulate market development in upgraded fuels, with long-term public sector supply contracts strengthening the business case for fuel supply investments.7

Boosting upgraded-fuel competitiveness:

- Consider making the VAT for sustainable renewable fuels lower than for coal, fuel oil and natural gas.

- Ensure that forestry residue feedstocks for upgraded fuels (e.g. wood chips or pellets) are provided at a suitable price to make the fuels more cost-competitive.

Increasing combustion efficiency:

- Establish education and outreach programmes that offer guidance on best-practice combustion to ensure that households continuing to use firewood at least do so as efficiently as possible.

- Support new efficient-stove production businesses through financial de-risking measures (e.g. grants, soft loans or fiscal measures) to facilitate investment in equipment.

Cross-cutting:

- Introduce appropriate standards and certification measures (e.g. for stove efficiency or fuel characteristics8) to improve end-user confidence and facilitate market development.

- Develop replicable exemplar pilot projects in public buildings capable of long-term operations, bringing together appropriate technologies, upgraded-fuel supplies and operational competences.

- Assess the feasibility of PPP energy service company (ESCO) business models for the provision of heat as opposed to fuels.

- Create a publicly available online platform to map areas of sustainable biomass resource availability and heating demand.

References

Trees planted, usually in rows, to provide shelter from the wind and to protect soil from erosion.

According to the Intergovernmental Panel on Climate Change (IPCC), methane’s global warming potential is 28 times that of CO2 over a 100-year timescale (UNFCCC, 2016).

EfW should be deployed according to its place in the wider waste management hierarchy of prevention, preparing for reuse, recycling, (energy) recovery and disposal.

An approximate increase from 10 MJ/kg to 14 MJ/Kg.

Based on a purchase cost of GEL 60 of a basic stove (25% efficiency) compared with an improved stove (45% efficiency) at GEL 300 or an efficient stove (75% efficiency) at GEL 500.

This assessment should build on existing end-use data collection on household energy consumption.

This approach should also deliver spillover benefits for residential sector supplies.

Fuel standardisation is becoming increasingly important with the introduction of more sophisticated heating appliances to the market.

Reference 1

Trees planted, usually in rows, to provide shelter from the wind and to protect soil from erosion.

Reference 2

According to the Intergovernmental Panel on Climate Change (IPCC), methane’s global warming potential is 28 times that of CO2 over a 100-year timescale (UNFCCC, 2016).

Reference 3

EfW should be deployed according to its place in the wider waste management hierarchy of prevention, preparing for reuse, recycling, (energy) recovery and disposal.

Reference 4

An approximate increase from 10 MJ/kg to 14 MJ/Kg.

Reference 5

Based on a purchase cost of GEL 60 of a basic stove (25% efficiency) compared with an improved stove (45% efficiency) at GEL 300 or an efficient stove (75% efficiency) at GEL 500.

Reference 6

This assessment should build on existing end-use data collection on household energy consumption.

Reference 7

This approach should also deliver spillover benefits for residential sector supplies.

Reference 8

Fuel standardisation is becoming increasingly important with the introduction of more sophisticated heating appliances to the market.