Cite report

IEA (2022), Energy Efficiency 2022, IEA, Paris https://www.iea.org/reports/energy-efficiency-2022, Licence: CC BY 4.0

Report options

Executive summary

Efficiency action accelerates as countries move to contain economic pain from the energy crisis

The unparalleled global energy crisis sparked by the Russian Federation’s (hereafter “Russia”) invasion of Ukraine has dramatically escalated concerns over energy security and the inflationary impact of higher energy prices on the world’s economies.

Lowering record-high consumer bills and securing reliable access to supply is a central political and economic imperative for almost all governments. While there are many ways for countries to address the current crisis, focusing on energy efficiency action is the unambiguous first and best response to simultaneously meet affordability, supply security and climate goals.

With efforts to conserve and better manage energy consumption in sharp focus since the onset of the crisis, efficiency progress has gained momentum, with annual energy intensity improvements expected to reach about 2% in 2022.

Annual global primary energy intensity improvement by scenario, 2001-2030

OpenGlobal energy demand growth has declined sharply and is expected to be close to 1% this year. This comes after last year’s 5% increase; one of the largest single-year rises in 50 years.

This year’s improvement in intensity comes after the onset of Covid-19 led to two of the worst years ever for global energy intensity progress, with annual gains falling to around half of one percentage point in 2020 and 2021. Key factors included a higher share of energy-intensive industry in energy demand and slower efficiency progress, especially in the buildings and industrial sectors.

However, energy intensity progress had already slowed before the start of the Covid-19 pandemic in 13 of the G20 group of countries and improved in only four. From 2010 to 2020, the global rate of improvement fell from 2% in the first half of the decade to 1.3% in the second half. This highlights the challenge of re-accelerating efficiency progress to the 4% needed each year to 2030 under the IEA Net Zero Emissions by 2050 Scenario (Net Zero Scenario).

With consumers reducing energy consumption in an effort to rein in costs, this year’s energy intensity improvement cannot entirely be viewed as a step forward. Businesses are under pressure to close or curtail operations and many people across the world are struggling to afford basic energy needs. The number of people without reliable access to heating, cooling, clean cooking and other energy services has risen to around 2.5 billion worldwide, and an extra 160 million households have been pushed into energy poverty since 2019.

High fossil fuel prices are driving a cost-of-living crisis, worsening energy poverty and public health

Energy price inflation varies across countries depending on the fuel mix, the level of energy efficiency and the structure of the economy, as well as government polices such as fuel taxation and energy bill support strategies. While the current crisis is global, it is centred in Europe where reduced energy supply from Russia is exposing consumers to higher energy bills and risks of supply shortages over the winter heating months.

In the European Union, consumer energy price inflation for the year to October 2022 increased to 39%, with around a quarter of households estimated to be living in energy poverty. Vulnerable groups are the most exposed and often live in older, poorer-quality buildings, using less efficient appliances and older vehicles with lower energy performance levels. This not only means they can be paying several times more for household energy bills but also suffer colder, damper, and darker living conditions which exacerbate health risks.

This year has also seen a significant shift back towards using cheaper traditional biomass such as wood and charcoal for heating and cooking. Emerging and developing economies are particularly exposed. Around 75 million people who have recently gained access to electricity are estimated to have lost the ability to pay for it and 100 million people may need to switch back to using traditional stoves for cooking from LPG. This poses a particular health risk for women and children who are most exposed to household air pollution from cooking which in total is estimated to have contributed to 2.5 million premature deaths this year.

Year-on-year change in energy price inflation, October 2022

OpenWell-targeted public spending can support the vulnerable and enhance efficiency

With households and businesses facing significantly higher energy bills this year, governments in all regions have brought forward a range of interventions to provide support for consumers, including new or increased broad-based fuel subsidies as well as direct cash payments to assist households. The value of this emergency government spending is now over USD 550 billion. In emerging and developing economies, this short-term support now eclipses that provided for clean energy investments since March 2020. Support is set to further increase substantially, such as through a proposed package in Germany of up to USD 200 billion.

In the transport sector the percentage of energy price increases being passed through to consumers has fallen across many countries with the difference between market prices and end-user prices usually being met from public budgets.

Proportion of transport fuel price increases passed through to consumers by region, Dec 2020 - Apr 2022

OpenWhile offering important short term relief, at the same time it is important such support does not weaken incentives to reduce energy waste or slow the switch to lower-carbon supply. The least efficient interventions are those that lower market prices for energy through direct fossil fuel consumption subsidies, indiscriminately applied to all consumers. Such subsidies risk removing the incentives to improve efficiency and disproportionately benefit wealthier consumers who are large energy consumers.

The IMF and the OECD have highlighted the need to scale down such broad-based energy subsidies and shift their balance towards targeted support for energy poverty and structural energy efficiency measures. Higher energy efficiency, which reduces energy consumption, also plays an important role in lowering the overall energy subsidy burden on public budgets in the longer term.

Energy efficiency spending tops USD 1 trillion, equal to two-thirds of all clean energy recovery packages

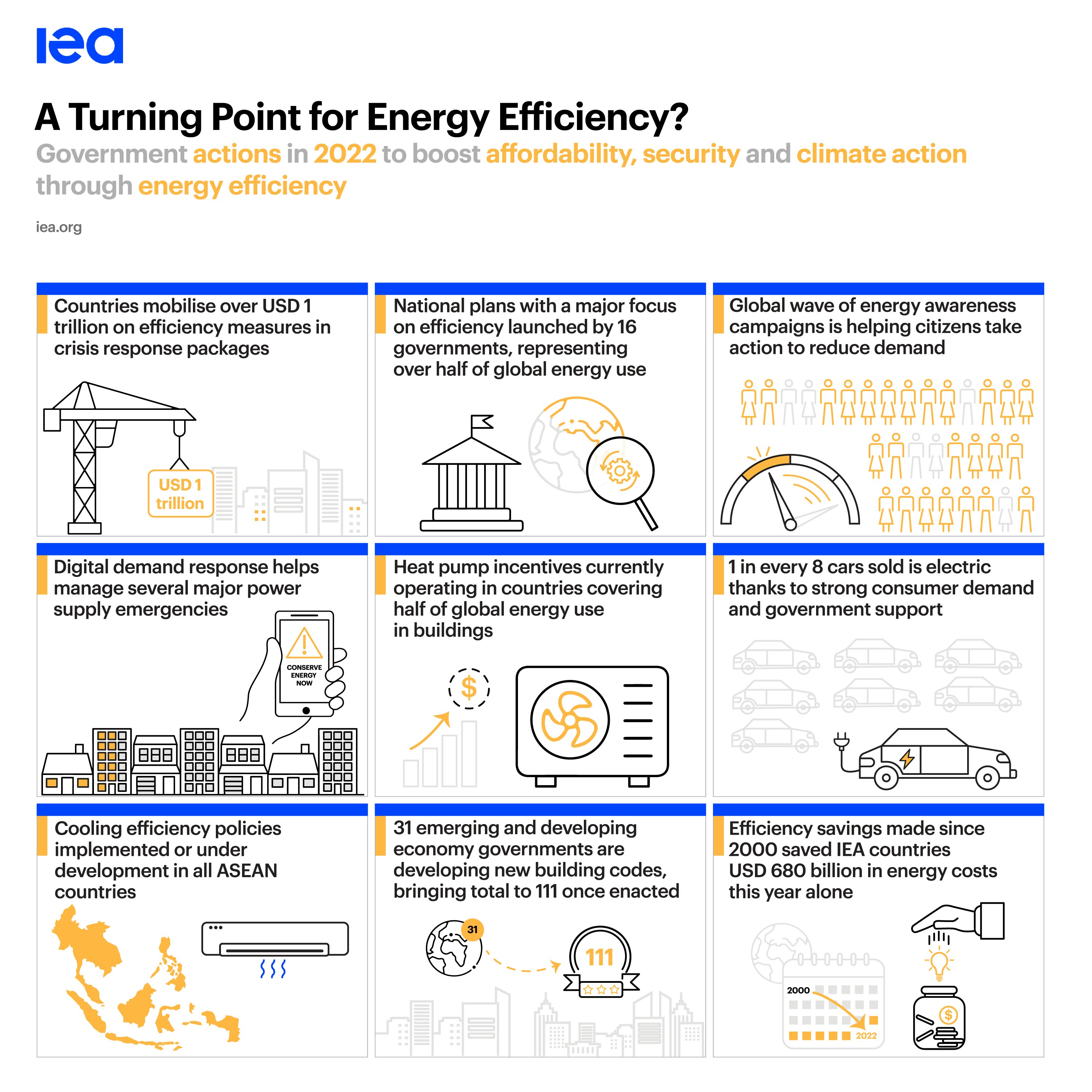

Since 2020, governments worldwide have helped mobilise around USD 1 trillion for energy efficiency-related actions such as building retrofits, public transport and infrastructure projects, and electric vehicle support. This amounts to approximately USD 250 billion a year being deployed from 2020 to 2023, equivalent to two-thirds of total clean energy recovery spending.

This is the result of USD 270 billion of direct public spending by governments, which is projected to mobilise a further USD 740 billion of private and other public spending. This provides a productivity boost to the economy and can contribute to minimising future energy-related cost-of-living pressures that may arise.

Global spending in clean energy and recovery, 2020-2023

OpenGlobal efficiency investment is up 16%, led by record growth in electric vehicle sales

Strong consumer spending on new fuel-efficient and electric cars is expected to help overall energy efficiency-related investment rise by 16% in 2022, to just over USD 560 billion. Under currently stated policies, this figure is set to increase a further 50% to almost USD 840 billion per year from 2026 to 2030. However, these levels are still only about half of the energy efficiency-related investment levels needed in the second half of this decade to align with the Net Zero Scenario.

Global efficiency-related transport investment is expected to rise 47% in 2022 to USD 220 billion. This includes just over USD 90 billion on electrification, which now makes up an estimated 42% of total efficiency-related transport investment, compared with just 19% in 2019. Growth in energy efficiency investment for buildings was down to 2% this year compared with 12% the year before as construction activity slowed and costs rose sharply from higher interest rates and supply chain pressures on materials and labour.

Electric vehicle sales have almost doubled for the last two years in a row, reaching around 11 million units sold worldwide in 2022, up from just 1 million in 2017. This means that electric cars now account for 13% of new vehicle sales worldwide. Conventional energy efficiency investment in the transport sector also performed strongly, rising by USD 33 billion or 35%, to USD 128 billion, driven by investment in more efficient vehicles.

Despite this record growth, there is evidence that supply chain constraints are restricting even faster progress. This relates particularly to the availability of semiconductor and lithium processing. Longer waiting lists are now widespread for many popular new electric vehicle models and the prices of second-hand electric vehicles are increasing.

Energy savings from past efficiency actions are lowering energy bills by USD 680 billion this year in IEA countries

With consumer energy expenditures strongly rising this year in most countries, the value of improving energy efficiency in reducing costs and saving energy has risen exponentially. Efficiency gains will help mitigate financial hardship for residential consumers and provide critical cost savings for commercial users struggling in a weaker global economy. But, to achieve these goals, it is essential that policy makers adopt well-targeted and broad sets of energy efficiency measures.

Over the last 20 years, IEA member countries have implemented energy efficiency-related measures across the buildings, industry and transport sectors that are estimated to be saving households and businesses around USD 680 billion this year, or around 15% of the total 2022 energy bill of USD 4.5 trillion. This reflects end-use energy prices for fuels in IEA countries this year and 24 EJ of avoided energy demand from efficiency-related measures.

Change in energy demand and drivers in IEA countries, 2000-2020

OpenThe accumulated effects of efficiency have been so large that final energy demand for IEA countries as a group has remained relatively steady at about 140 EJ for 20 years. This was achieved even as the economies of the group grew by 40% in real terms and overall economic structure only slightly shifted towards less energy-intensive activities.

Stronger efficiency is the first-best policy to bring down energy bills

There is a wide range of energy efficiency performance levels in homes, offices, businesses and vehicles. For example, evidence suggests that the reduction in running costs between the most efficient and least efficient homes or cars can be commonly as much as 40% and up to 75% depending on the initial level of efficiency. This means that it can cost some consumers two or even three times more to heat the same area or travel the same distance.

Variations in energy efficiency exist both within and among countries. For example, in some European countries with similar climates it can take twice as much energy to heat the same floor area or within one country the energy consumed between the most efficient and least efficient homes for a given size can vary by a factor of up to three.

Typical annual household energy bills by building energy performance certificate rating, in the United Kingdom at summer 2019 and October 2022 prices

OpenFor transport, the differences in vehicle age, efficiency levels, size and fuel type have a major impact on annual fuel bills, as does the choice of travel mode. For example, the most efficient vehicles of the same size and weight use around half the energy of the same type of vehicle purchased ten years ago. Analysis of personal vehicles in Europe suggests a new compact electric car is by far the cheapest vehicle to run, with typical annual energy costs around half that of the most efficient new non-EV compact car.

Fuel bills for different personal vehicle types in Europe, June 2021-June 2022

OpenMore efficient buildings will play a key role in enabling Europe to achieve independence from Russian gas

Natural gas is the most common fuel currently used globally for residential heating, accounting for 42% or 760 bcm of heating energy needs. Within Europe, gas dependency for heating ranges from over 80% in the Netherlands to almost total independence in some countries such as Norway and Sweden.

As a consequence of the current energy crisis, the share of Russian gas in total European demand has fallen from 47% in 2019 to around 9% in 2022. This loss of supply has precipitated an acute energy security crisis, given the limited availability of alternative affordable natural gas, and has brought into focus the pressing need for greater diversification of supply sources and routes.

In most countries across Europe, the price of gas relative to electricity for households has risen significantly. This has dramatically changed the economics of heating. For example, in Denmark, the cost of operating a gas heating system has risen for an average household by around 330% whereas the cost to heat the same space with an electric heat pump has risen by around 100%. While relative prices vary across Europe, efficient electric heat pumps are now the clear leader when it comes to the operating costs of heating most buildings.

A growing number of countries and sub-national governments have legislation underway proposing bans or phase-out schedules for gas and oil heating appliances. Across the European Union and the United Kingdom seven countries accounting for 80% of residential gas use in the region plan to ban new gas heating connections.

Proportion of residential heating energy consumption by fuel source in selected countries, 2020

OpenFor example, Germany plans to put in place an implicit ban on new fossil fuel heating from 2024, when all newly-installed heating systems must be supplied by at least 65% renewable energy. France plans to ban new gas connections to buildings from 2023, Austria intends to implement a ban from 2023 and the Netherlands will require heat pump installations or heat network connections in buildings from 2026. The United Kingdom has announced plans to prohibit new gas heating systems and boilers by 2025, and ban them for all buildings by 2035.

In the United States, a small number of states have legislation underway proposing bans on new fossil fuel heating. In September 2022 California moved to bring in regulations which prohibit sales of gas-powered space and water heaters from 2030. Over 60 cities in California have already announced bans or are actively discouraging gas use in buildings. Oregon already outlawed natural gas use in any new construction since 2021. In Canada, the city of Vancouver and the province of Quebec also have plans to ban hot water systems powered by fossil fuels.

The largest energy efficiency opportunities of the future will be found in emerging and developing countries

Emerging market and developing economies (EMDEs) together account for around 260 EJ or 60% of global final energy demand. While the rate is slowing in many countries, under current policy settings final energy demand by 2030 is expected to grow almost 20% to around 305 EJ. This will increase EMDEs’ global share by 5% as energy demand in advanced economies is expected to stay relatively steady.

Percentage change in annual average final energy demand in selected emerging market and developing economies countries, 2000-2019

OpenBehind this energy growth story is a rise in energy consumption per person in EMDEs as incomes grow. For example, an average person in an EMDE currently uses three times less energy in their home and four times less energy for transport, compared with an average person in an advanced economy.

With emerging countries accounting for an ever-greater share of energy demand, the largest energy efficiency opportunities will increasingly be found in such countries as Brazil, the People’s Republic of China (hereafter “China”), India, Indonesia, Mexico and South Africa. Given their critical importance to global energy security and climate goals, the IEA collaborates with these countries and others in Africa, the ASEAN and Latin American regions to support energy efficiency through its Energy Efficiency in Emerging Economies (E4) programme.

Historic moment for international cooperation on efficiency to help secure affordable clean energy

Not since the founding of the IEA in 1974 has the need for a coordinated effort on energy efficiency to reduce wasteful and inefficient use of energy been so great. No other energy resource can compare with energy efficiency as a solution to the energy affordability, security of supply and climate change crises. This is why the IEA calls energy efficiency the “first fuel” of all energy transitions.

In June 2022, the IEA held its 7th Annual Global Conference on Energy Efficiency in Sønderborg, Denmark. This was the largest ever gathering of ministers from countries around the world to specifically discuss the value of stronger action on energy efficiency. At the conference 26 governments issued a joint statement “calling on all governments, industry, enterprises and stakeholders to strengthen their action on energy efficiency” and welcoming the Sønderborg Action Plan on Energy Efficiency. This plan outlines a set of strategic principles and policy toolkits developed by the IEA that can help governments implement efficiency policies rapidly.

Is 2022 likely to be a turning point for energy efficiency?

A key question for policy makers right now is whether the energy crisis will bring about a global turning point for accelerating much-needed energy efficiency progress over this decade following the recent weak performance. The step up in energy intensity improvements from less than half a percentage point during each of the previous two years to almost 2% in 2022 is encouraging, though weaker-than-expected economic growth or higher energy consumption could still see this figure reduced by 0.3%. It is also only half of the 4% of annual intensity improvements needed, on average, over this decade to align with the Net Zero Scenario. And while there are causes for optimism, significant headwinds to faster progress remain.

{kind=link}

{kind=link}

The events of 2022 have nonetheless changed the dynamics of energy markets for decades to come. In the wake of these disruptions, energy efficiency has received a series of major global boosts:

- Global energy efficiency investment is increasing fast, with governments, industry and households investing USD 560 billion this year, which is a new record.

- Energy efficiency-related spending is making up two-thirds of all clean energy and recovery spending, with USD 1 trillion mobilised since 2020. At least 16 high profile national plans are driving this progress on efficiency, including the US Inflation Reduction Act, the REPowerEU Plan and Japan’s Green Transformation (GX) Initiative.

- A rising wave of energy saving awareness campaigns is helping millions of citizens better manage energy use and make efficiency-related decisions.

- Existing building codes are being strengthened and new ones are being introduced in emerging and developing countries. Cooling strategies are being introduced in regions with the fastest-growing demand for air conditioning.

- The electrification of transport and heating looks to have reached a turning point. One in every eight cars sold globally is now electric, while almost 3 million heat pumps were sold in 2022 in Europe alone as they become the preferred heating option.

- The value that energy efficiency brings to consumers increased dramatically this year given sharply higher prices. While energy cost-of-living pressures have risen considerably, efficiency actions implemented over the last 20 years are now saving consumers in IEA countries USD 680 billion off their energy bills this year at current prices.

Despite these welcome causes for optimism several barriers to faster progress remain:

- There has been a massive scale-up of fossil fuel subsidies as governments seek to cushion the impact of higher energy prices on household bills. Over USD 550 billion of temporary support has been added over the last year. If support is not well targeted, this could weaken the case for energy efficiency.

- Energy efficiency investment is highly concentrated in advanced economies. If global efficiency improvements are to accelerate, investment and polices covering the other 60% of energy consumption in EMDEs must be strengthened.

- The Covid-19 crisis saw a shift towards more energy-intensive industry. Energy efficiency progress will continue to be stymied if strong industrial demand for energy persists without a major improvement in industrial energy efficiency.

- Much of the energy demand reduction that has taken place may be a negative consequence of slowing business, or consumers forgoing energy services to save money. Short-term efforts to save energy can easily revert back to past patterns of behaviour once the crisis eases.

In the midst of a global polycrisis, energy efficiency’s role as the “first fuel” has been underscored by its ability to simultaneously meet energy affordability, security and climate goals. Efficiency actions reduce overall energy demand, putting downward pressure on energy prices and CO2 emissions, generating employment and lowering bills for consumers.

The conditions are in place for 2022 to become a turning point year for energy efficiency progress. Governments worldwide are acting to strengthen their economies, helping struggling citizens and boosting businesses through energy efficiency action. But to capitalise on this opportunity and accelerate progress, it will be crucial that they continue to put in place more targeted, sustained and broader sets of measures.