IEA (2021), Ammonia Technology Roadmap, IEA, Paris https://www.iea.org/reports/ammonia-technology-roadmap, Licence: CC BY 4.0

Executive Summary

Ammonia makes an indispensable contribution to global agricultural systems through its use for fertilisers. Ammonia is the starting point for all mineral nitrogen fertilisers, forming a bridge between the nitrogen in the air and the food we eat. About 70% of ammonia is used for fertilisers, while the remainder is used for various industrial applications, such as plastics, explosives and synthetic fibres. While the use of ammonia as a fuel shows promise in the context of clean energy transitions, this application currently remains nascent. The focus of this roadmap is therefore on existing agricultural and industrial uses of ammonia.

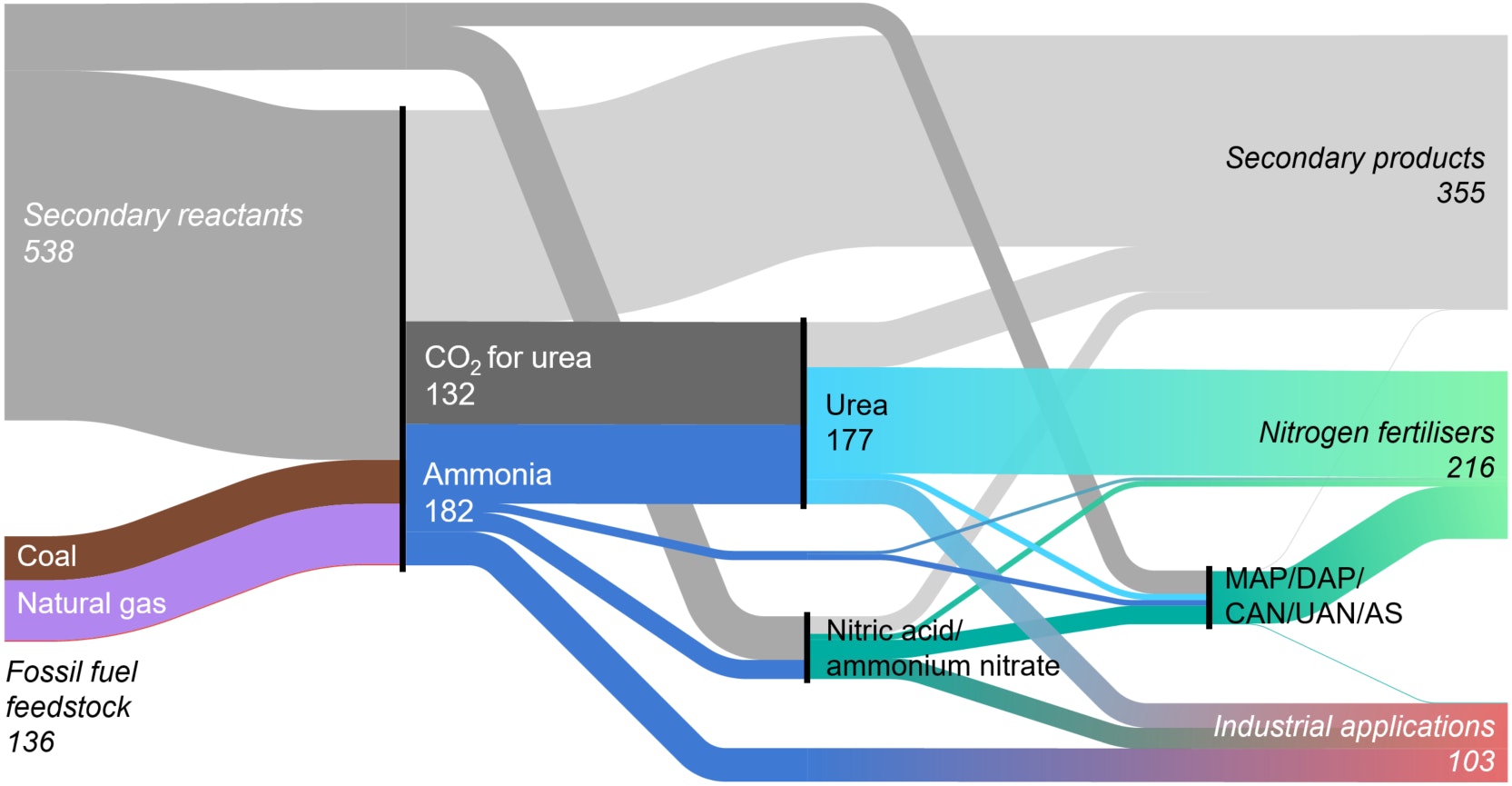

Mass flows in the ammonia supply chain: from fossil fuel feedstocks to nitrogen fertilisers and industrial product

Open

{kind=link}

In the future, the world will need more ammonia but with fewer emissions. An increasingly numerous and affluent global population will lead to growth in ammonia demand, during a period in which governments around the world have declared that emissions from the energy system must head towards net zero. This technology roadmap explores three possible futures for ammonia production. In the Stated Policies Scenario the industry follows current trends, making incremental improvements but falling well short of a sustainable trajectory. In the Sustainable Development Scenario the sector adopts the technologies and policies required to put it on a pathway aligned with the goals of the Paris Agreement. The Net Zero Emissions by 2050 Scenario describes a trajectory for the ammonia industry that is compatible with the energy system reaching net zero emissions globally by 2050.

An energy- and emissions-intensive global industry

Ammonia production currently relies heavily on fossil fuels. Global ammonia production today accounts for around 2% (8.6 EJ) of total final energy consumption. Around 40% of this energy input is consumed as feedstock – the raw material inputs that supply a proportion of the hydrogen in the final ammonia product – with the rest consumed as process energy, mainly for generating heat. Just over 70% of ammonia production is via natural gas-based steam reforming, while most of the remainder is via coal gasification, leading to 170 bcm of natural gas demand (20% of industrial natural gas demand) and 75 Mtce of coal demand (5% of industrial coal demand). Oil and electricity combined account for just 4% of the sector’s energy inputs.

Ammonia production is emissions intensive. Direct emissions from ammonia production currently amount to 450 Mt CO2 – a footprint equivalent to the total energy system emissions of South Africa. Indirect CO2 emissions are around 170 Mt CO2 per year and stem from two main sources – electricity generation and the chemical reaction that takes place when urea-based fertilisers are applied to soils. Ammonia is one of the most emissions-intensive commodities produced by heavy industry, despite coal accounting for a much smaller share of its energy inputs than in other sectors. At around 2.4 t CO2 per tonne of production, it is nearly twice as emissions intensive as crude steel production and four times that of cement, on a direct CO2 emissions basis.

Energy and emission intensities for key industrial products, 2021

OpenAmmonia is produced and traded around the world. China is the largest producer of ammonia, accounting for 30% of production (and 45% of CO2 emissions), with the United States, the European Union, India, Russia and the Middle East accounting for a further 8-10% each. Ammonia is traded around the world, with global exports equating to about 10% of total production. Urea, its most common derivative, is traded even more widely, at just under 30% of its production. The availability of feedstock and process energy is a key determinant of where and how ammonia is produced. Low-cost natural gas in the United States, Middle East and Russia explain the prominent roles of these regions and their natural gas-based plant fleets. China’s abundant coal reserves explain its heavy reliance on the fuel, which accounts for around 85% of its production.

Absent a change in course, ammonia production would continue to take an environmental toll

The industry’s current trajectory is unsustainable. In the Stated Policies Scenario, ammonia production increases by nearly 40% by 2050, driven by economic and population growth. CO2 emissions grow by 3% by 2030, before entering a decline that is mainly spurred by increases in energy efficiency and a decline in the proportion of coal use. In 2050, emissions are 10% lower than today. Cumulative direct emissions from ammonia production under current trends amount to around 28 Gt between now and 2100, equivalent to 6% of the remaining emissions budget associated with limiting global warming to 1.5 °C.

Existing assets give the industry’s emissions momentum. Ammonia production facilities have long lifetimes of up to 50 years. The current average age of installed capacity is around 25 years since first installation, but this figure is subject to significant regional variation. Plants in Europe are around 40 years old on average, compared with 12 years in China, which is home to around 30% of global capacity. Depending how long these plants operate, the existing global stock could produce up to 15.5 Gt CO2 over their remaining lifetime, which is the equivalent of 35 years’ worth of ammonia production emissions in 2020.

Projected emissions from existing ammonia plants under different lifetime assumptions, 2020-2070

OpenNon-CO2 environmental impacts should not be neglected. In addition to CO2 emissions, the production of nitrogen fertilisers also results in nitrous oxide emissions. Nitrous oxide and CO2 are also generated in the use phase during and after fertiliser application. While exact quantities are hard to measure accurately, it is estimated that use-phase emissions are upwards of 70% of the total life-cycle greenhouse gas emissions of nitrogen fertilisers. The over-application of mineral fertilisers can damage ecosystems, but the higher crop yields enabled by fertilisers can also reduce the conversion of natural ecosystems to agricultural production. Methane emissions generated during the extraction and transport of fossil fuels pose a further challenge – as they do for the energy system more broadly – but order-of-magnitude reductions can be achieved with commercially available technologies, a significant proportion of them at zero net cost.

Towards more sustainable ammonia production

Encouraging progress on near-zero-emission technologies is already being made. Near-zero-emission production methods are emerging, including electrolysis, methane pyrolysis and fossil-based routes with carbon capture and storage (CCS). These emerging routes are typically 10-100% more expensive per tonne of ammonia produced than conventional routes, depending on energy prices and other regionally varying factors. Existing and announced projects totalling nearly 8 Mt of near-zero-emission ammonia production capacity are scheduled to come online by 2030, equivalent to 3% of total capacity in 2020.

Two pathways outline a range of desirable futures for the ammonia industry. In the Sustainable Development Scenario, direct CO2 emissions fall by over 70% by 2050 relative to today. The Net Zero Emissions by 2050 Scenario describes a trajectory where emissions fall by 95% by 2050. The difference between the components of these scenarios is one of degree, not of direction.

Direct CO₂ emissions from ammonia production, 2020-2050

OpenUsing ammonia more efficiently – reducing demand growth without compromising the end-use services it provides – eases the burden on technology deployment. Slower growth in total production is the outcome of strategies such as increasing the efficiency of nitrogen fertiliser application and increased recycling and re-use of plastics and other durable ammonia-derived goods. By 2050, ammonia production in the Sustainable Development Scenario and Net Zero Emissions by 2050 Scenario is 10% lower than in the Stated Policies Scenario.

Using technology to improve the performance of existing equipment is important, but alone is not sufficient to deliver the emission savings required. The global average energy intensity of ammonia production today is around 41 GJ/t on a net basis, compared with best available technology (BAT) energy performance levels of 28 GJ/t for natural gas-based production and 36 GJ/t for coal-based production. The universal adoption of BAT, in combination with operational improvements and a structural shift in the processes used to produce ammonia, together yield a reduction of around 25% in the average energy intensity of production by 2050 in the Sustainable Development Scenario and the Net Zero Emissions by 2050 Scenario.

Near-zero-emission ammonia production requires new infrastructure, innovation and investment

The heavy lifting with respect to emission reductions is done by deploying near-zero-emission technologies. Their deployment contributes the largest share of emission reductions in both the Sustainable Development Scenario and Net Zero Emissions by 2050 Scenario. In the Sustainable Development Scenario, the share of near-zero-emission technologies reaches nearly 70% of total production1 by 2050, up from less than 1% today. Natural gas-based production equipped with CCS accounts for around 20% of production, while for electrolysis the share of total production is more than 25%. In the Net Zero Emissions by 2050 Scenario, near-zero-emission technologies achieve nearly 95% of total production by 2050. Natural gas-based production with CCS accounts for around 20% of production, and electrolysis for more than 40%.

Global ammonia production by technology and scenario, 2020-2050

OpenMost near-zero-emission technologies are not yet available at commercial scale in the marketplace. CO2 separation is an inherent part of commercial ammonia production, but permanent storage of the CO2 is not yet widely adopted. Electrolysis-based ammonia production has already been conducted at scale using high-load-factor electricity, but challenges remain in the use of hydrogen produced from variable renewable energy (such as solar PV and wind) directly in captive installation arrangements. Nearly 60% of the cumulative emission reductions in the Sustainable Development Scenario stem from technologies that are currently in the demonstration phase.

New infrastructure must be deployed at a rapid clip. The Sustainable Development Scenario requires more than 110 GW of electrolyser capacity and 90 Mt of CO2 transport and storage infrastructure by 2050. This means installing on average ten 30 MW electrolysers (the largest facility in operation today) per month and 1 large capture project (annual capture, transport and storage capacity of 1 Mt CO2) every four months between now and 2050. In the Net Zero Emissions by 2050 Scenario, the additional emission reductions require an even more rapid deployment of these technologies.

Overall investment needs for a sustainable pathway are roughly equivalent to those associated with current trends. The Sustainable Development Scenario requires USD 14 billion in annual capital investment for ammonia production to 2050. Of this, 80% is in near-zero-emission production routes. The Net Zero Emissions by 2050 Scenario requires only slightly higher annual investment – USD 15 billion to 2050. In the Sustainable Development Scenario, it is only after 2040 that the investment per tonne of ammonia produced increases above that of the Stated Policies Scenario. Prior to 2040, the avoidance of continued capital-intensive investment in coal-based production in China yields significant savings, and the lower quantity of ammonia produced yields further savings in overall investment needs.

Enabling more sustainable ammonia production

The industry is primed for change. Governments, producers and other stakeholders have already begun taking action to reduce emissions from the ammonia industry. Some governments have adopted carbon pricing regimes and are funding innovation, while producers have set emission reduction targets and are undertaking RD&D projects. Despite these efforts, emissions continue to rise, and greater ambition is needed.

Governments’ role is central. Governments will need to establish a policy environment supportive of ambitious emission cuts by creating transition plans underpinned by mandatory emission reduction policies, together with mechanisms to mobilise investment. Targeted policy is also required to address existing emissions-intensive assets, create markets for near-zero-emission products, accelerate RD&D and incentivise end-use efficiency for ammonia-based products. Governments should ensure that enabling conditions are in place, including a level playing field in the global market for low-emission products, infrastructure for hydrogen and CCS, and robust data on emissions performance.

Other stakeholders also have a crucial part to play. Ammonia producers will need to establish transition plans, accelerate RD&D, and engage in initiatives to develop supporting infrastructure. Farmers and agronomists should prioritise best management practices for more efficient fertiliser use. Financial institutions and investors should use sustainable investment schemes to guide finance towards emission reduction opportunities. Researchers and non-governmental organisations can help develop labelling schemes, continue research on early-stage technologies and galvanise support for key technologies.

Time is of the essence. The current decade – from now to 2030 – will be critical to lay the foundation for long-term success, with around 10% of cumulative emission reductions to 2050 taking place by then in both the Sustainable Development Scenario and Net Zero Emissions by 2050 Scenario. Vital near-term actions include establishing strong supportive policy mechanisms, taking early action on energy and use efficiency, developing supporting infrastructure, and accelerating RD&D.

References

Calculated excluding the portion equipped with carbon capture for providing CO2 for urea production.

Calculated excluding the portion equipped with carbon capture for providing CO2 for urea production.