Bioenergy with Carbon Capture and Storage

What is BECCS?

Bioenergy with carbon capture and storage, or BECCS, involves capturing and permanently storing CO2 from processes where biomass is converted into fuels or directly burned to generate energy. Because plants absorb CO2 as they grow, this is a way of removing CO2 from the atmosphere.

What is the role of BECCS in clean energy transitions?

Bioenergy with carbon capture and storage is the only carbon dioxide removal technique that can also provide energy. Because bioenergy can provide high-temperature heat and fuels that work in existing engines, BECCS plays an important role in decarbonising sectors such as heavy industry, aviation and trucking in the Net Zero Emissions by 2050 Scenario.

Where do we need to go?

While encouraging, plans for BECCS deployment remain insufficient across all sectors to get on track with the Net Zero Scenario. Development of the necessary infrastructure to transport and store the captured CO2 also lags behind what is needed in this scenario, despite growing support in recent years.

Bioenergy with carbon capture and storage, or BECCS, involves capturing and permanently storing CO2 from processes where biomass is converted into fuels or directly burned to generate energy. Because plants absorb CO2 as they grow, this is a way of removing CO2 from the atmosphere.

Bioenergy with carbon capture and storage is the only carbon dioxide removal technique that can also provide energy. Because bioenergy can provide high-temperature heat and fuels that work in existing engines, BECCS plays an important role in decarbonising sectors such as heavy industry, aviation and trucking in the Net Zero Emissions by 2050 Scenario.

While encouraging, plans for BECCS deployment remain insufficient across all sectors to get on track with the Net Zero Scenario. Development of the necessary infrastructure to transport and store the captured CO2 also lags behind what is needed in this scenario, despite growing support in recent years.

Tracking Bioenergy with Carbon Capture and Storage

Not on track

Bioenergy with carbon capture and storage (BECCS) involves any energy pathway where CO2 is captured from a biogenic source and permanently stored. Only around 2 Mt of biogenic CO2 are currently captured per year, mainly in bioethanol applications. Plans for around 20 facilities together capturing around 15 Mt CO2 per year of biogenic emissions have been announced since January 2022.

Based on projects currently in the early and advanced stages of deployment, carbon removal via BECCS could reach just under 50 Mt CO2/yr by 2030, which falls far short of the approximately 190 Mt CO2/yr removed through BECCS by 2030 in the Net Zero Emissions by 2050 (NZE) Scenario. Targeted support for carbon dioxide removal (CDR), and BECCS in particular, will be required to translate recent momentum into operational capacity.

US policies continue to support development of carbon capture, utilisation and storage and targeted BECCS programmes emerge in Europe

Countries and regions making notable progress to advance BECCS include:

- Denmark, where two combined heat and power plants with the capacity to remove more than 0.4 Mt CO2 per year by 2026 were awarded a contract by the Danish Energy Agency in May 2023 as part of the carbon capture, utilisation and storage (CCUS) subsidy scheme. The same agency is also consulting market participants for a DKK 2.6 billion (EUR 350 million) subsidy scheme targeted at negative emissions (the Negative Emissions CCS [NECCS] fund).

- The United States announced major increases to the 45Q tax credit for CCUS in 2022 under the Inflation Reduction Act, which supports BECCS by providing tax credits now valued at USD 60 per tonne of CO2 used and USD 85 per tonne of CO2 stored.

- The United Kingdom launched its Hydrogen BECCS Innovation Programme in 2022, which plans to issue more than GBP 30 million in funding over two phases to support technologies that can produce hydrogen from biogenic feedstocks that are combined with carbon capture. In parallel, a public consultation on business models for BECCS in power was also launched in July 2022.

Despite increasing awareness around the importance of BECCS for reaching net zero, deployment remains low

BECCS and direct air capture (DAC) with CO2 storage are technology-based solutions for CDR, required to meet net zero ambitions. BECCS is the only CDR technique that can also provide energy. Biogenic sources used for BECCS can be process emissions resulting from biofuel and biohydrogen production, or combustion emissions from heat and power generation in power plants, waste-to-energy plants and industrial applications fired or co-fired by biomass (cement, pulp and paper) or using biochar as a reducing agent (steel). As an alternative to storage, the captured CO2 can also be utilised as a feedstock for a range of products. While some carbon capture and utilisation routes can bring important climate benefits, CO2 removal can only be achieved through permanent storage.

Around 2 Mt CO2 per year are currently captured from biogenic sources, with less than 1 Mt CO2 stored in dedicated storage. Around 90% is captured in bioethanol facilities, one of the lowest-cost BECCS applications due to the high concentration of CO2 in the process gas stream. The largest operating BECCS project to date is the Illinois Industrial CCS Project, which has been capturing CO2 for permanent storage in a deep geological formation since 2018. The Red Trail Energy bioethanol project, the second in the United States targeting dedicated storage, came online in 2022. Other small-scale bioethanol facilities are capturing CO2 in Europe and the United States, but these either sell the CO2 to greenhouses for yield boosting or use it for enhanced oil recovery.

While bioethanol is currently the leading BECCS application, more projects in power and industry are expected to come online

Around 40 additional bioethanol facilities are planned to come online before 2030 (including around 30 as part of the Midwest Carbon Express project in the United States), totalling around 15 Mt of biogenic CO2 capture capacity.

Project announcements in the past two years suggest that the BECCS project pipeline is diversifying, with proportionally more capture projects being announced in heat and power, hydrogen and cement:

- Around 20 Mt of biogenic CO2 could be captured from heat and power plants, with over 80% from dedicated biopower plants, and the remainder from waste-to-energy plants. In Denmark, two combined heat and power plants were awarded a contract by the Danish Energy Agency in 2023 as part of its CCUS subsidy scheme.

- In industry, six cement plants have announced plans to integrate biomass feedstock in the clinker production process and retrofit CCUS. Most cement plants planning to use biomass and carbon capture and storage aim to be at best carbon neutral, rather than carbon negative, due to either partial capture rates or partial biomass substitution for fossil fuels. These include the Brevik Norcem plant in Norway currently under construction, the Cementa Slite plant in Sweden and the K6 Lumbres project in France.

- Four projects are also targeting CCUS retrofits at pulp and paper mills, with two plants announced in 2022 in Canada.

- There are plans for two hydrogen facilities to run partly or fully on biomass with CCUS.

While encouraging, plans for BECCS deployment remain insufficient across all sectors to get on track with the NZE Scenario. By 2030, in that scenario around 40 Mt/yr is removed in the power sector, 130 Mt/yr in the fuel transformation sector and 20 Mt/yr in industry, mainly cement, with nearly 190 Mt captured in total – around 4 times higher than the ~50 Mt in the project pipeline.

Targeted support will also be required to ensure all projects in planning reach commissioning. Around 15% of total planned BECCS capacity hinges on the Drax power plant in the UK securing governmental support, after their shortlisted 8 Mt CO2 per year project was not selected in the government cluster sequencing Track-1 project list. The company nonetheless continues to lead BECCS developments, with two new facilities in the United States with a cumulative capture capacity of 6 Mt CO2 per year by 2030 announced in May 2023, and more projects under evaluation.

Lead times for BECCS projects depend heavily on the application and destination of the CO2

Project experience in bioethanol and biopower plants equipped with CCUS suggests that project lead times on the capture side can range from 1.5 to 6.5 years, averaging 3.5 years. However, lead times depend strongly on the application and destination of the CO2. The only two plants involving storage that are in operation today – both bioethanol plants in the United States – took around seven years to complete (including the construction of transport and storage infrastructure). In contrast, projects involving the use of captured CO2 were completed in less than four years.

Bioethanol plants tend to involve shorter lead times than bio-based power applications. Lead times can be as short as one to two years for bioethanol plants, as they only require the installation of CO2 drying and compression units, which are less capital-intensive than full capture units. Given that current facilities are first- or second-of-a-kind, lead times will most likely shorten as deployment increases. In the United States, the lead time for retrofitting the second bioethanol facility with CCS was one year shorter than for the first.

As the deployment of CO2 transport and storage infrastructure is currently an important bottleneck, the deployment of large CCUS hubs can help accelerate lead times for BECCS facilities in the longer term. Given the long lead times involved in the deployment of large CO2 management infrastructure, investment decisions are needed in the next couple of years to get on track with deployment in 2030 envisaged in the NZE Scenario.

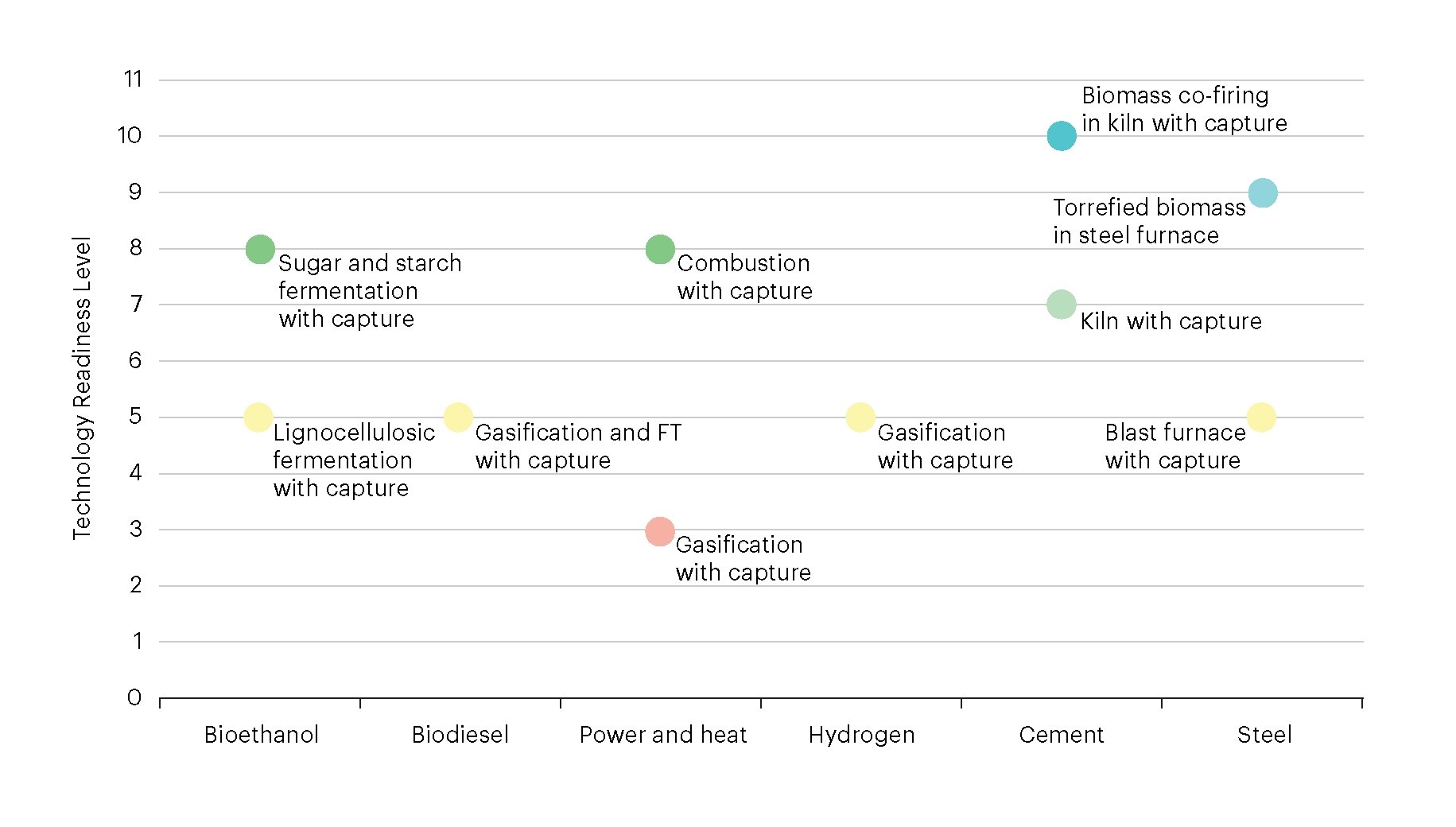

Some BECCS routes are commercial, but the most critical are still at the demonstration or pilot stage

CO2 capture from first-generation bioethanol production is the most mature BECCS route, with operations dating back to the late 2000s. CO2 capture at biomass combustion plants has been at the commercial demonstration stage since October 2020 with the commissioning of a capture unit at Mikawa power station in Japan, but large-scale gasification of biomass for synthetic gas applications is still at the large prototype stage.

In industry, biomass co-firing is already commercial in pulp and paper mills, cement plants, and steel blast furnaces. However, CO2 capture from kilns and blast furnace off-gas is still at the prototype or demonstration stage, though the world’s first commercial CO2 capture unit on a cement kiln is under construction, for commissioning in 2024.

Technology readiness level of selected BECCS pathways

Open

{kind=link}

Innovation in capture and biomass conversion technologies can make BECCS more effective

Chemical absorption is the state-of-the-art capture method, but other capture technologies with a lower energy requirement are at various stages of development. UK power company Drax has been piloting a solid-adsorption capture pilot using metal organic frameworks in its North Yorkshire incubation hub since March 2022. Work to demonstrate large-scale biomass gasification for synthesis gas applications is also under way, seeking to reduce capital costs and increase feedstock flexibility. Projects include one on woody biomass for biomethane production in Sweden, and one on waste in the United Kingdom.

Targeted subsidy programmes and certification frameworks are supporting BECCS

Policy approaches to CDR solutions require a high degree of transparency to demonstrate clear climate benefits and ensure trust from stakeholders. Internationally recognised frameworks are needed to support the integration of CDR, including BECCS, into existing regulations.

To that end, in November 2022 the European Commission proposed an EU-wide voluntary framework to certify high-quality carbon removals. The proposal sets out rules for the independent verification of removals, as well as rules to recognise certification schemes that can be used to demonstrate compliance with the EU framework. The proposed regulation establishes four criteria to ensure high-quality removals:

- Quantification

- Additionality

- Long-term storage

- Sustainability

In Denmark, the NECCS Fund provides up to DKK 2.6 billion (EUR 350 million) in subsidies to support negative emissions from CO2 capture of biogenic sources and subsequent geological storage, with the aim of achieving negative emissions of an additional 0.5 Mt per year from 2025 onwards. Since the launch of the programme in 2022, the Danish Energy Agency has invited market participants to provide input into the tender process.

In the United Kingdom, the Hydrogen BECCS Innovation Programme aims to support technologies that can produce hydrogen from biogenic feedstocks that are combined with carbon capture. Under the first of two phases, in August 2022 the government provided GBP 5 million (USD 6.2 million) in funding to over 20 projects aimed at delivering commercially viable technology solutions across three categories: feedstock preprocessing, gasification components and novel biohydrogen technologies. In December 2022, up to GBP 25 million (USD 31 million) in funding was announced under the second phase of the programme to take projects from innovation design through to innovation demonstration.

Investment in BECCS is growing across applications

Funding is targeting the RD&D of various BECCS applications, as well as specific commercial projects:

- In the European Union, two large-scale projects involving biogenic capture were selected for funding under the EU’s Innovation Fund 2021 funding call: the HySkies sustainable aviation fuel project sourcing CO2 from a combined heat and power plant in Sweden (EUR 80 million) and the Go4ECOPlanet cement project in Poland (EUR 228 million).

- In Denmark, the first tender of the CCUS subsidy scheme released in May 2023 awarded funds to a 0.4 Mt per year BECCS project that is planning to capture CO2 at two biomass-fired power stations for dedicated storage.

- In Canada, Emissions Reduction Alberta announced nearly CAD 2.5 million (USD 1.9 million) in funding in 2022 to study the capture and storage of biogenic CO2 emissions at West Fraser’s Hinton Pulp Mill site, permanently removing 1.3 Mt CO2 per year.

We would like to thank the following external reviewer:

Jasmin Kemper, IEA Greenhouse gas R&D programme (IEAGHG), Reviewer

Recommendations

Authors and contributors

Lead authors

Mathilde Fajardy

Carl Greenfield

Recommendations