Carbon Capture, Utilisation and Storage

What is carbon capture, utilisation and storage (CCUS)?

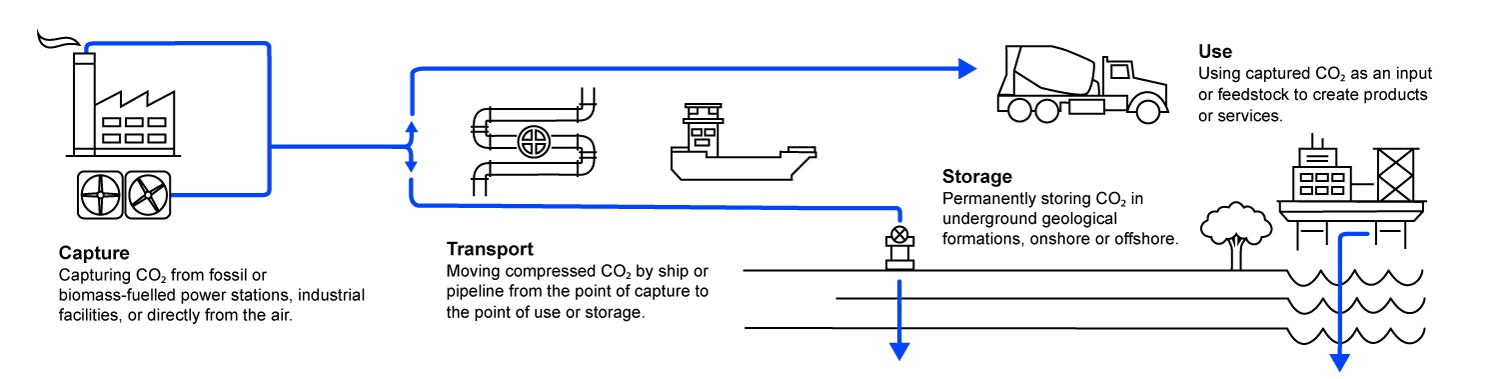

CCUS involves the capture of CO2, generally from large point sources like power generation or industrial facilities that use either fossil fuels or biomass as fuel. If not being used on-site, the captured CO2 is compressed and transported by pipeline, ship, rail or truck to be used in a range of applications, or injected into deep geological formations such as depleted oil and gas reservoirs or saline aquifers.

What is the role of CCUS in clean energy transitions?

CCUS can be retrofitted to existing power and industrial plants, allowing for their continued operation. It can tackle emissions in hard-to-abate sectors, particularly heavy industries like cement, steel or chemicals. CCUS is an enabler of least-cost low-carbon hydrogen production, which can support the decarbonisation of other parts of the energy system, such as industry, trucks and ships. Finally, CCUS can remove CO2 from the air to balance emissions that are unavoidable or technically difficult to abate.

Where do we need to go?

CCUS deployment has been behind expectations in the past but momentum has grown substantially in recent years, with over 500 projects in various stages of development across the CCUS value chain. Nevertheless, even at such level, CCUS deployment would remain well below what is required in the Net Zero Scenario.

In this sector

How does CCUS work?

A visual overview of each step in the CCUS process.

{kind=link}

Tracking Carbon Capture, Utilisation and Storage

Around 40 commercial facilities are already in operation applying carbon capture, utilisation and storage (CCUS) to industrial processes, fuel transformation and power generation. CCUS deployment has trailed behind expectations in the past, but momentum has grown substantially in recent years, with over 500 projects in various stages of development across the CCUS value chain. Since January 2022, project developers have announced ambitions for around 50 new capture facilities to be operating by 2030, capturing around 125 Mt CO2 per year. Nevertheless, even at such a level, CCUS deployment would remain substantially below (around a third) the around 1.2 Gt CO2 per year that is required in the Net Zero Emissions by 2050 (NZE) Scenario.

The United States and Europe issue billions in funding for projects, while Germany and Japan make significant progress on CCUS legislation

Countries and regions making notable progress in CCUS include:

- The United States announced important opportunities in 2023 that are expected to boost CCUS project development, including USD 1.7 billion for carbon capture demonstration projects and USD 1.2 billion for direct air capture (DAC) hubs under the 2021 Infrastructure Investment and Jobs Act.

- The European Union issued around USD 1.5 billion to CCUS projects under the latest Innovation Fund round, and over USD 500 million to CO2 transport and storage projects under its Connecting Europe Facility programme. Other notable funding for CCUS projects occurred in the Netherlands (USD 7.3 billion) and Demark (USD 1.2 billion). This is boosting project development, including first Dutch transport and storage project Porthos reaching a final investment decision (FID) to start injecting 2.5 Mt CO2 per year in offshore gas fields in 2027, while injection for the first phase (25 kt CO2 per year) of the Ravenna CCS hub in Italy is set to start in 2024. Additionally, FIDs were reached for five capture facilities across application including in ammonia and for two hydrogen facilities in the Netherlands, and in bioenergy with CCUS in Denmark.

- Germany made its re-entry into CCUS with the release of its carbon management strategy that identifies CCUS as a crucial to meeting the country’s carbon neutrality ambitions by 2045. In addition to the strategy, the government plans to amend legislation to allow for the regulation of CCUS activities, including offshore CO2 storage.

- Japan is quickly advancing its CCUS efforts with the selection of seven large-scale projects to capture and store around 13 Mt CO2 per year in 2030. It is also progressing on its draft CCS Business Act, which will establish a legal framework for CCUS across the value chain, and proposal to amend the London Protocol to allow for the transboundary storage of CO2.

CCUS facilities currently capture more than 50 Mt CO2 annually

There are now around 45 commercial capture facilities in operation globally, with a total annual capture capacity of more than 50 Mt CO2. Close to ten large-scale (capture capacity over 100 000 tCO2/year, and over 1 000 tCO2/yr for DAC applications) capture facilities entered operation in 2023, including the Blue Flint ethanol project, Linde Clear Lake capture facility, and Heirloom and Global thermostat’s first 1,000 tCO2/yr facilities in the United States, and four projects in China (the Jiling Petrochemical CCUS facility, the CNOOC Enping oil field, the first phase of the Guanghui Energy CCUS integration project and the China Energy Taizhou power plant). It also includes the capture facility at the Petra Nova plant in the United States, which restarted operations after a 3-year suspension. While planned capacity for 2030 increased by around 2030 since last year, the pipeline of current projects is only just around 40% of the Net Zero Scenario requirement in 2030.

Capacity of current and planned large-scale CO2 capture projects vs. the Net Zero Scenario, 2020-2030

OpenMomentum is growing in applications that are key for reaching net zero but actual final investment decisions are lagging behind

Momentum behind CCUS has been growing since around the start of 2018. Since February 2023 project developers have announced ambitions for 115 Mt CO2 per year of additional capture capacity 2030.1

1. Specific CO2 transport and storage related activities and progress are reported in CO2 Transport and Storage.

Evolution of the CO2 capture project pipeline, 2012-Q1 2024

OpenCurrently, around 65% of operating CO2 capture capacity is at natural gas processing plants, one of the lowest-cost CO2 capture applications, but the widespread adoption of economy-wide decarbonisation targets for 2050 is stimulating the diversification of CO2 capture applications towards sectors that are key to reaching net zero. These include hard-to-abate industries, the power sector, the production of low-emissions hydrogen and ammonia, and atmospheric carbon dioxide removal. Based on the current project pipeline, by 2030 annual capture capacity from both new construction and retrofits could amount to around 95 Mt CO2 from hydrogen production, around 90 Mt CO2 from power generation, around 50 Mt CO2 from industrial facilities (e.g. cement and steel production), and around 65 Mt CO2 from DAC plants.

Announcements are however just the first step: whether all projects materialise continues to be an open question. As of February 2024, capture capacity that is either already in operation or has reached FID still accounts for just 20% of announced capture capacity for 2030. Two-thirds of FIDs taken in 2023 involved these use cases, versus only 40% in 2022. But greater ambition is needed in some sectors – particularly industry, which currently makes up less than 10% of announced capacity. It would need to reach a quarter of all of CO2 captured by 2030 in the Net Zero Scenario.

Plans for CO2 capture facilities are expanding globally

The geographic distribution of CO2 capture projects in development is diversifying, with projects now being developed in more than 50 countries. Beyond North America and Europe, good progress has also been made in:

- Asia Pacific (including China), four new capture facility started operations in China in 2023, and planned capture and storage capacity could reach 50 Mt CO2 and 85 Mt CO2 per year by 2030, respectively.

- The Middle East, where around 15 projects are in development across the region in addition to the three already in operation. In 2023, two CO2 transport and storage hubs were announced in Bahrain and in the United Arab Emirates, and ADNOC reached a FID on the construction of a 1.5 Mt CO2 per year capture facility at Habshan-Bab gas plant.

Promising technological innovations are being demonstrated around the world

Several technological innovations that have been proposed to reduce CCUS costs for power generation are now being tested:

- NET Power’s 50 MW clean energy plant (commissioned in 2018) is a first-of-its-kind natural gas-fired power plant employing Allam cycle technology, which uses CO2 as a working fluid in an oxyfuel supercritical CO2 power cycle, which could significantly reduce capture costs.

- Net Zero Teesside Power in the United Kingdom is expected to come online in 2027 and could become one of the first commercial-scale gas-fired power stations with CCUS. The project was named as an investment priority in a UK government announcement in March 2023.

- A large-scale demonstration capture unit was also retrofitted at the Taizhou coal power plant in China, with the capacity to capture 0.5 Mt CO2 per year.

While the most advanced and widely adopted capture technologies are chemical absorption and physical separation, other separation technologies under development include membranes and looping cycles (such as chemical looping and calcium looping).

In addition to technology improvements, different trends could further improve the techno-economic performance of CO2 capture. Examples include modularisation of capture systems within self-contained, plug-in systems (with the potential to reduce land footprint, costs and lead times of capture retrofits across applications) and hybridisation of different capture technologies within capture systems (to increase capture rates while reducing costs and/or energy penalty).

Higher CO2 capture rates are possible and will be needed for net zero systems

Higher CO2 capture rates will be essential for CCUS to play its role in the transition to a net zero energy system. CCUS-equipped power and industrial plants operating today are designed to capture around 90% of the CO2 from flue gas. While there are no technical barriers to increasing capture rates beyond 90% for the most mature capture technologies, capture rates of 98% or higher require larger equipment, more process steps and higher energy consumption per tonne of CO2 captured, which increases unit costs. However, initial results based on chemical absorption systems applied to power generation plants are promising, showing that CO2 capture rates as high as 99% can be achieved at comparably low additional marginal cost relative to the cost of deploying 90% capture.

Governments focus on public funding, strategic signalling and cross-border collaboration on CCUS

- Public funding: Government funding for CCUS continued in 2023 as ongoing subsidy programmes in the United States and Europe made over USD 20 billion available to CCUS projects. This includes the USD 1.7 billion that was made available to carbon capture demonstration projects and the USD 1.2 billion for DAC hubs promised under the 2021 Infrastructure Investment and Jobs Act in the United States. In the Netherlands, the SDE++ scheme allocated over USD 7.3 billion to CCS projects that will connect to the massive Aramis CO2 transport and storage network. In Demark, Ørsted received USD 1.2 billion from the CCUS Fund for its capture retrofit project on the Asnæs Power Station. On top of individual country-level funding, the European Commission also issued around USD 1.5 billion to CCUS projects in the industry sector under the latest Innovation Fund round, and over USD 500 million to CO2 transport and storage projects under its Connecting Europe Facility programme.

- Strategic signalling: With renewed recognition of the need to collectively do more on CCUS, 2023 saw the creation of significant new initiatives. Launched at the Major Economies Forum in April 2023, the Carbon Management Challenge features a joint call to action for governments to accelerate the deployment of CCUS technologies. In early 2024, Bahrain became the newest signatory to the Challenge, which includes 20 countries and the European Commission. Several countries have also advanced strategic plans to support CCUS. For example, Canada finalised its Carbon Management Strategy at the end of 2023, while the European Commission released its Industrial Carbon Management Strategy in early 2024, which sets out a comprehensive policy approach to help the European Union develop at least 50 Mt of capacity by 2030 and 280 Mt by 2040. Other European countries, including France and Germany, are simultaneously developing their own strategies.

- Cross-border collaboration: In some regions, countries are looking to one another to collaborate on cross-border CCUS projects. Such is the case in the North Sea, where Denmark, Belgium, the Netherlands and Sweden each established an arrangement on cross-border transport of CO2 with Norway in April 2024, making it possible to transport and store CO2 between the countries. Sweden and Denmark concluded a similar arrangement. In March 2024, Denmark and France signed a similar arrangement. Such deals are required under the London Protocol, an international agreement that regulates the cross-border transport of CO2 for offshore storage. Japan, which is actively progressing on amending the London Protocol, is also pursuing opportunities to export its captured CO2, with two of its seven government-supported CCS projects geared to ship CO2 from Japan to Southeast Asia. To this end, in September 2023 Japan signed a memorandum of co-operation with Malaysia’s national oil company, PETRONAS, on the transboundary transport and storage of CO2.

View all carbon capture, storage and utilisation policies

We would like to thank the following external reviewers:

- Abdul'Aziz A. Aliyu, Technology Collaboration Programme on Greenhouse Gas R&D/IEAGHG

- Keith Burnard, Technology Collaboration Programme on Greenhouse Gas R&D/IEAGHG

- Tim Dixon, Technology Collaboration Programme on Greenhouse Gas R&D/IEAGHG

- Nirvasen Moonsamy, Oil and Gas Climate Initiative

- Rachael Moore, CO2 Management Solutions.

Recommendations

-

CCUS hubs can spread infrastructure costs between emitters and generate economies of scale to reach emitters that are smaller-scale or further away from identified CO2 storage sites. Governments can have a key role in the development of hubs by:

- Co-ordinating hub development through competitive solicitations that encourage collaboration across multiple sectors (e.g. industrial emitters, power plants). Efforts are already underway in Canada, the United States, and the United Kingdom.

- Ensuring legal and regulatory frameworks are designed to account for shared infrastructure networks that allow for non-discriminatory open access and outline cost-sharing requirements.

-

CCUS projects are large infrastructure endeavours that can take up to ten years to be developed, involving multiple stakeholders and often several regulatory regimes that lengthen the amount of time it takes to start operation. If left unaddressed, long lead times for CCUS can put short-term climate targets at risk, making it more challenging and costly to achieve long-term goals. Governments can accelerate administrative and permitting procedures by:

- Establishing a clear permit approval timeline and requirement framework for CCUS projects.

- Designating one regulatory agency as a one-stop-shop for all permitting activities that can co-ordinate all the necessary requirements.

- Building regulatory support capacity by ensuring regulatory bodies are adequately resourced. It is vital that they are equipped with sufficient funding, staff and expertise to oversee the implementation of CCUS regulations.

-

Well-targeted policies and a portfolio of measures can help ensure government efforts to support CCUS deployment are effective and successful in the long term.

Governments can signal their strategic interest in CCUS through the inclusion of CCUS in national energy and climate strategies – for example, the EU Net Zero Industry Act identifies CCUS as a key strategic net zero technology – or in their Nationally Determined Contributions under the Paris Agreement. The creation of national or regional CCUS targets can help signal strategic interest.

Governments can also create an enabling environment for CCUS projects, such as through the establishment of a carbon pricing system; capital grants to reduce up-front costs; loans and loan guarantees to provide access to debt capital; and tax credits to address capital and operating costs.

Importantly for higher-cost CCUS applications, such as in the power, cement and steel sectors, governments have a range of different policies to spur initial deployment: R&D funding to reduce costs; carbon contracts-for-difference to provide a predictable revenue stream to operators, and public procurement programmes for low-emission products/fuels to spark demand.

-

New business models and deployment approaches for CO2 management are emerging and can facilitate rapid CCUS scale-up. These include: building multi-user CO2 management infrastructure; developing “as-a-service” business models for CO2 capture, transport and storage wherein each part of the chain is offered as third-party operated services; and exploiting new and existing options for CO2 use to provide a revenue stream to CCUS facilities.

Moving from full-chain to part-chain projects will require much higher levels of cross-industry co-ordination, especially as interest in CCUS hubs grows. In addition to working closely with governments, the private sector can establish industry consortia or coalitions to facilitate co-ordination on ensuring the efficient build-out of hubs.

Programmes and partnerships

A worldwide database of CCUS projects

Explore the IEA's database of carbon capture, utilisation and storage projects. The database covers all CCUS projects commissioned since the 1970s with an announced capacity of more than 100 000 t per year (or 1 000 t per year for direct air capture facilities) and a clear scope for reducing emissions.

Authors and contributors

Lead authors

Sara Budinis

Mathilde Fajardy

Carl Greenfield